HSBC Malta announces special dividend after 9-year absence

HSBC Bank Malta plc kicked-off the financial reporting season last week with the publication of its 2017 annual financial statements.

The bottom-line figure should not have surprised the market. HSBC Malta reported a 9.5% drop in adjusted pre-tax profits to €55.6 million, reflecting lower revenues due to the negative interest rate environment and the change in the business model in recent years coupled with higher operating costs mainly due to increased regulatory obligations.

At the interim stage in June 2017, HSBC had in fact announced a 15% decline in adjusted pre-tax profits. Furthermore, in the Interim Directors’ Statement published on 20 November 2017, the bank had explained that between 1 July and 15 November 2017, it continued to suffer a decline in profitability when compared to the same period last year.

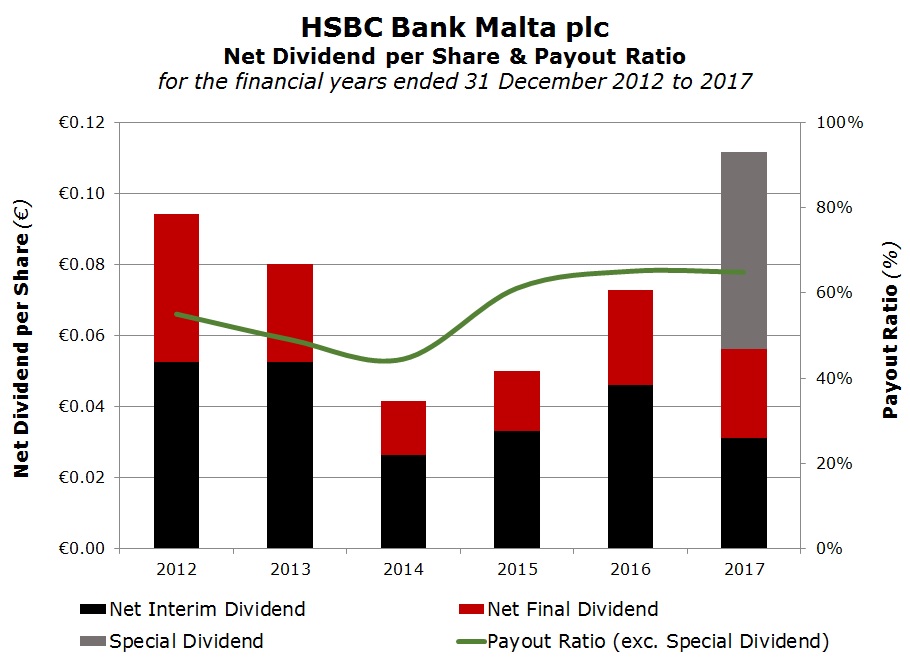

Notwithstanding the drop in profits, the Directors of HSBC are recommending the payment of a €20 million special dividend in addition to the customary ordinary dividend based on a 65% payout ratio. HSBC Malta are recommending that at the upcoming Annual General Meeting, shareholders approve an ordinary net dividend of €0.0251 per share as well as a special net dividend of €0.0555 per share. The total net final dividend of €0.0806 per share will then be paid on 19 April 2018 to all shareholders as at close of trading on Friday 9 March 2018.

Investors who have held HSBC Malta shares for several years may recall a series of special dividends some time ago. In fact, HSBC Malta adopted an aggressive dividend policy between 2004 and 2007. Special dividends were distributed in respect of each of these four financial years over and above the ordinary dividends. At the time, HSBC had increased its ordinary dividend payout ratio from 50% in 2004 to 75% for the following three years.

Although the special dividend announcement caught many investors by surprise, investors who follow the local capital market closely would have been alerted by some of the remarks made by the bank on 20 November 2017.

HSBC Malta re-introduced the publication of the semi-annual Interim Directors’ Statement in the second half of last year and in part of its commentary in the announcement on 20 November, it stated that the bank “commenced a review to assess how best to deploy this capital going forward”. This was undoubtedly the most important statement in the announcement and it was a very clear precursor to last week’s special dividend recommendation. This once again indicates the importance of the publication of Interim Directors’ Statements twice a year and all other companies should contemplate issuing such announcements once again to ensure that the market is regularly updated on company developments.

HSBC Malta is one of the very few companies that convenes a meeting for analysts and the press on the same day of the publication of their financial statements. During the presentation on 20 February, HSBC Malta’s CEO Mr Andrew Beane gave a detailed overview of the change in the bank’s business model over recent years which translated into the strong capital position it has today and enabled the bank to not only sustain a dividend payout ratio of 65% but to also pay an extraordinary dividend out of retained earnings.

Mr Beane argued that the strategy over the past few years was centred around a lower risk business model in order to meet the highest global standards for compliance and risk management. The CEO explained that HSBC made enormous progress in the quality of risk management and implemented world-class customer due diligence procedures. Following the period of the significant repositioning of the bank, the new 3-year strategy approved by the Board of Directors last week focuses on a clear customer-led strategy to grow profitability over time without increasing risk. Mr Beane also indicated that HSBC Malta will continue to focus on rewarding shareholders appropriately as a result of the strong capital position and the excess liquidity.

HSBC’s CEO also made reference to the “somewhat different business model to Bank of Valletta plc”. In fact, the different strategies and business models should be very clear to many local investors given the requirement for a €150 million rights issue by BOV on the one hand late last year compared to the generation of a significant amount of additional capital by HSBC Malta in recent years which triggered the €20 million special dividend.

In last week’s presentation, Mr Beane also made two other very important remarks. The CEO issued a very clear warning that although Malta’s economy continues to perform well, damage was done to the jurisdiction and in order to ensure sustainable and broad-based economic growth, it is essential to safeguard the reputation of the jurisdiction and achieve international compliance standards across the industry. Despite the positive assessments being received by various rating agencies over recent weeks and months, the statements by HSBC Malta’s CEO should not be taken lightly by all stakeholders.

The CEO of HSBC Malta also remarked about the “increasing level of long-term risk in the local bond market”, which he said had become a “greater cause for concern”. Mr Beane specifically mentioned “changes in the composition of the bond market”. I believe this remark is a specific reference to the Prospects market. In one of my articles last year, I had explained the important difference between the regulated main market and Prospects. Investors need to be highly aware of the significant difference between issuers on both markets especially with the growing pipeline of new issues in the weeks and months ahead.

Moreover, it is also equally important for investors to be in a position to distinguish between the stronger issuers (which have low gearing ratios and higher interest cover) and those companies with weak financial metrics who may have difficulty in honouring their obligations should the economic performance weaken or should they fail to achieve their financial projections.

In order to assist investors to be in a position to gauge the strength of the various bond issuers on the regulated main market, I had published a series of articles during the month of December to highlight the important metrics and developments across the various issuers. It is very important for investors to obtain assistance to understand the strength of each of the issuers not only at the time of a new issue but also during the lifetime of the bond. A very good example in this respect is the developments at 6pm Holdings plc. The serious shortcomings highlighted in the 2016 Annual Report and the 2017 interim financial statements which were published very late indeed and which led to a very long period of suspension in trading on the bonds to the detriment of the holders of such bonds, should also be an eye-opener and should not be easily forgotten by the investing public.

While it is important that the bond market continues to provide investors with opportunities to diversify their investment portfolios, it is equally important that the growth of the market is managed in a well-structured manner. The remarks made by the CEO of HSBC calls for an open dialogue between all market participants together with the MFSA as the regulator of the entire financial services industry and also government representatives to ensure a sustainable capital market develops with a high level of corporate governance standards.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.