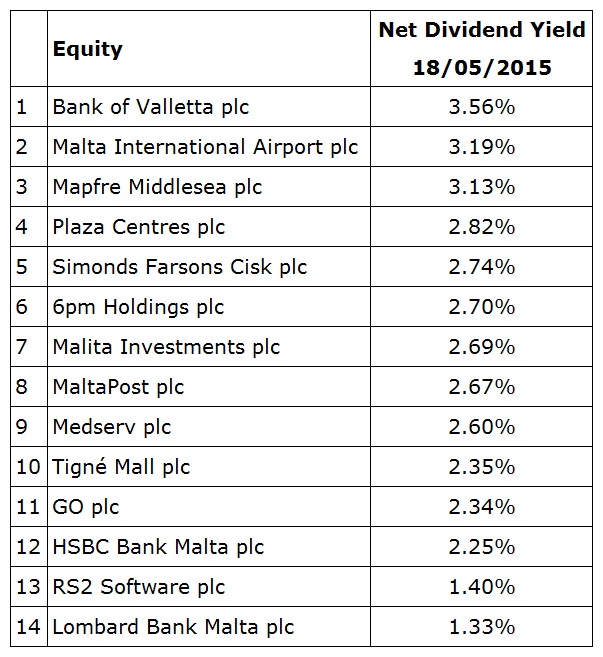

The 2015 Dividend League Table

An article on the dividend league table has now become an annual event following the conclusion of the annual financial reporting season on 30 April.

The dividend league table is based on the net dividend yield and not the gross yield by each of the companies in their last annual financial year. This provides a better comparison across the market since some companies benefit from tax incentives and distribute dividends out of tax free profits.

The 2015 dividend league table therefore is based on the net dividend distributed to shareholders in respect of the 2014 financial year with the resultant yield calculated on the current market price of the respective shares.

A comparison of the 2015 league table with that published last year provides some interesting observations due to a number of developments that took place over the past 12 months.

As a start, it is worthwhile noting that yields are generally substantially lower than last year mainly as a result of the significant rally in many share prices but also as a result of some lower dividend payments. This is mainly the case with the banks.

Notwithstanding the 22% decline in the overall dividend paid by Bank of Valletta plc last year, the Bank retained the top spot in the league table. However, the net yield is now at 3.6% compared to 5.3% last year – a very clear indication of the considerable decline in yields over the last 12 months.

Malta International Airport plc moved up seven places in the league table from 9th position in 2014 to 2nd position in 2015. The current net yield of 3.2% is however marginally lower than last year’s net yield of 3.3% as the 47% increase in the dividend paid out in respect of the 2014 financial year was offset by the sharp rally in the share price from €2.25 in May 2014 to the current level of €3.46, an increase of 53%. The bulk of these gains materialized in Q1 2015 following the significant increase in the final dividend and the forecast of further passenger growth expected during 2015.

The third place in the 2015 dividend league table goes to Mapfre Middlesea plc with a net yield of 3.1% compared to a net yield of 3.8% last year which had positioned Mapfre Middlesea in 6th positon in 2014. The company maintained its dividend payment unchanged but the 36% rally in the share price resulted in a lower yield.

The net yield of Simonds Farsons Cisk plc was one of the few that improved over the past twelve months. The net yield improved marginally to 2.8% but the ranking of Farsons improved to fourth place from 10th place in 2014. The 19% increase in the dividend paid out for the financial year to 31 January 2015 outweighed the 17.5% increase in the share price. Although the Farsons equity produced a double-digit gain, it underperformed most of the other market constituents largely as a result of the lack of supply of shares on the market due to the tight ownership structure which restricts trading activity.

The property related companies with business models capable of offering regular and sustainable dividends to shareholders have very different rankings in the league table largely as a result of different dividends declarations last year. Meanwhile, all three companies saw their share prices climb by over 50% last year. The highest yielding equity among the group is that of Plaza Centres plc as the company increased its dividend by 12.6% over last year following an improved financial performance on higher occupancy levels within the centre. Despite this improved dividend, the yield declined by almost 100 basis points from 3.8% in May 2014 to the current yield of 2.8% following the rally in the share price of 52%. Notwithstanding the decline in the yield, Plaza improved its ranking to 4th position in the league table.

Malita Investments plc dropped two positions in the league table as the dividend only increased marginally from one year to the next while the share price jumped by 58% – the second best performing equity over the past 12 months. The significant upturn in the share price led to a sizeable decline in the yield to 2.7% from 4.1% last year.

On the other hand, the 2.3% net yield of Tigne Mall plc was marginally unchanged from one year to the next as the 52% increase in the share price matched the increase in the dividend. The substantial increase in the dividend from one year to the next was due to the inclusion of the interim dividend in 2014 for the first time following the Initial Public Offering in the second half of 2013. Tigne Mall should continue with its semi-annual dividend distribution policy also in 2015 and future years.

The company that registered the largest increase in its overall dividend was Medserv plc with a rise of 133% from €0.024 per share to €0.056 per share. However, this equity was also the one that performed strongest over the past twelve months with a rally of 66%. The increase in the dividend outweighed the rise in the share price leading to an improvement in the yield from 1.85% in May 2014 to the current level of 2.60%. The strong increase in the yield helped Medserv improve its ranking from 13th place in 2014 to 9th place. Last Friday Medserv issued its 2015 financial projections and the Directors anticipate pre-tax profits rising by a further 33% during the current financial year to €4 million. The substantially higher dividend being approved by shareholders during the upcoming Annual General Meeting could therefore be sustainable in respect of the 2015 financial year given the expectation of the growth in profitability.

RS2 Software plc doubled its dividend from one year to the next while its share price increased by 32.5% resulting in an improvement in the net dividend yield from a mere 0.9% to 1.4%. Despite the doubling of the dividend, RS2 still ranks among the weakest dividend yielders in thirteenth place. On the other hand, the dividend paid by HSBC Bank Malta plc dropped by 48% and the yield declined from 4.2% to 2.25%. HSBC’s equity dropped from third positon in the 2014 dividend league table to a current ranking of twelfth in the 2015 table.

As was evident again last year, investors must not only base their investment decisions on the dividend yield of any particular year but on the sustainability of the divided in future years which is in turn dependent on individual company circumstances.

Moreover, investors would do well to understand that movements in bond yields as discussed in last week’s article, may also impact the equity market. As share prices of some companies rallied as a direct consequence of the sharp decline in bond yields over the past 12 months, any possible rally in yields in the coming months and years could likewise negatively impact some share prices. Notwithstanding this possible impact as a result of changing yield expectations, company-specific developments such as higher earnings from new business contracts or from acquisitions could also largely affect share price dynamics. In view of these multiple factors that influence share price movements, investors need to keep well abreast of market and company developments and seek regular independent financial advice to ensure that their portfolios are well structured to benefit from such developments whilst remaining within their investment objectives and risk levels.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.