Romanian acquisition boosts profitability of Premier Capital

Last week’s article reviewed the recent financial performance and developments at PTL Holdings plc – one of the three bond issuers within the Hili Ventures group of companies.

The other two issuers are Premier Capital plc and Hili Properties plc. Premier Capital plc had issued €25 million worth of bonds in March 2010 at a rate of 6.8% per annum. The bonds were issued for a maximum period of 10 years with an early repayment option after 7 years. As such, Premier Capital may redeem its bonds with effect from 16 March 2017.

Premier Capital is the development licensee for McDonald’s in Malta, Greece, Latvia, Lithuania, Estonia and, as from 22 January 2016, also Romania.

The purpose of today’s article is to review Premier Capital’s interim financial statements for the first half of 2016 which were published on 30 August.

On 22 January 2016, Premier Capital acquired a 90% shareholding in McDonald’s Romania for a total consideration of €63 million. At the time of the acquisition, there were 66 restaurants in operation in 21 cities across Romania and since then a further restaurant has been added to the portfolio. The 2015 Annual Report of Premier Capital published on 29 April 2016 stated that the acquisition was financed partly via a bank loan of €40 million and the balance of €23 million via an equity injection by the parent company, Hili Ventures Limited.

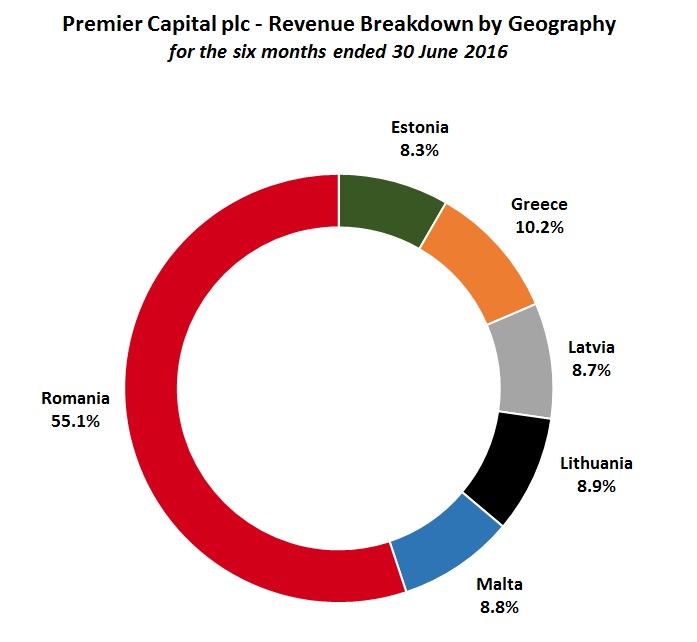

The 2016 first half results therefore include the initial contribution resulting from the Romanian investment. During the six-month period to 30 June 2016, Premier Capital plc generated total revenue of €103.2 million. This incorporates all the turnover across the portfolio of restaurants in Malta, Greece, Latvia, Lithuania, Estonia and Romania. The more interesting aspect of the June 2016 interim financial statements is the contribution from the restaurants across Romania.

The 2016 half-year report shows that the revenue from Romania amounted to €56.9 million. This represents 55% of overall revenue across Premier Capital which is a clear signal of the size and importance of this acquisition to the overall performance of Premier Capital. As such, the contribution from the restaurants in other countries has been diluted significantly. For example, until the acquisition in Romania, the restaurants in Malta contributed roughly just over 20% of overall revenue to Premier Capital. However, given the addition of 67 restaurants to the portfolio of Premier Capital, the importance of the Maltese operation in terms of revenue contribution has been diluted to below 9%. Naturally, the impact on the contribution across other countries was similar.

The performance of Premier Capital plc is therefore now very dependent on the performance of McDonald’s Romania.

More importantly, from a profitability aspect, the contribution from the Romanian operation is even more interesting. The segmental analysis published in the 2016 half-year report reveals that the subsidiary in Romania generated a pre-tax profit of €6.3 million between the date of acquisition on 22 January and 30 June 2016. This represents a pre-tax profit margin of 11.1%, which is far superior to that made in other countries. From an overall profitability aspect, the restaurants in Romania contributed almost 95% of the profits of Premier Capital during the first half this year. As such, the acquisition conducted earlier this year was a very important development for Premier Capital since it generated a very high level of profitability for the Group.

In last week’s article, I had mentioned some key highlights of the interim results of PTL Holdings plc and also compared these to the full-year projections prepared by the company. In the case of Premier Capital plc, however, this is not possible. Since Premier Capital launched a bond issue well before the Listing Policies came into effect in March 2013, there is no requirement for the company to publish its projections on an annual basis via the Financial Analysis Summary.

Although there are no detailed projections available for investors, Premier Capital plc Chairman Mr Melo Hili revealed in an interview published in the media on 31 January 2016, that Premier Capital aims to achieve a Group turnover of €230 million in 2016. Given the results achieved in the first half of the year with revenue amounting to €103 million, this seems achievable. One must take into account the seasonality aspect of the business in some countries (namely Malta and Greece) as well as the contribution for a full six-month period from Romania as opposed to just over 5 months in the first half of the financial year. Given the sizeable restaurant portfolio and the strong performance in Romania, the contribution for an additional 3 weeks is indeed material. In fact, the 2016 half-year report also indicates that had the acquisition in Romania taken place with effect from 1 January 2016 (instead of 22 January), overall Group revenues would have increased to €110 million (an additional €6.9 million) and pre-tax profits would have amounted to €4.8 million (an additional €0.7 million). Yet again, this proves how beneficial the acquisition in Romania has been for the Group.

The bondholders of Premier Capital should also be comforted by the improved financial metrics following the acquisition. Although the Group took on a further €40 million in debt funding (bringing overall borrowings to €82.5 million), the gearing ratio actually improved to 66% as a result of the shareholders’ injection of €23 million as well as the profits generated during the first six months of 2016. Moreover, the interest cover also improved substantially to over 6 times in the first half of 2016.

In the same interview published earlier this year, Mr Hili argued that besides Romania, the other markets which he believes have the greatest potential for further growth are Greece and Lithuania. Meanwhile, Premier Capital’s Directors also re-iterated in the 2016 half-year report that “there is significant business expansion opportunity in all the six markets in which it operates”. They argue that this can be achieved both in terms of growth from existing restaurants as well as from new restaurants across the various markets.

The sizeable acquisition by Premier Capital earlier this year has therefore already proved to be a very beneficial one from the initial results achieved to date. In the next few months, Premier Capital may avail itself of the option of an early repayment of its €25 million bond issue. Should this early repayment be financed by the issuance of new bonds, Premier Capital may be obliged to prepare financial forecasts which would be a welcome development from a market perspective. Meanwhile, given the recent strong financial performance, Premier Capital may also be one of the many local companies that would qualify for an equity listing in the near future. It is companies such as Premier Capital that are needed to help the local equity market become a more interesting investment medium for the growing number of investors seeking to invest via the Malta Stock Exchange.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.