Analysis of MGS take-up

In my article published 3 weeks ago entitled “Outlook for Malta’s capital market”, I questioned whether the Treasury of Malta will target the retail market for some of the new Malta Government Stock issuance throughout the rest of the year given the upturn in yields, or whether the new securities will be targeted again at institutional investors only.

The day after the publication of the article on 30 June, the Treasury very coincidentally announced the issue to both retail investors as well as to institutional investors of 3 new MGS for a total aggregate amount of €150 million subject to an over-allotment option of up to a further €100 million. The offer period for retail investors was last week between Monday 11 July and Wednesday 13 July, whilst the tender process for institutional investors closed on Friday 15 July at noon. On Friday afternoon, the Treasury published all the details of the take-up by both retail as well as the institutional investors.

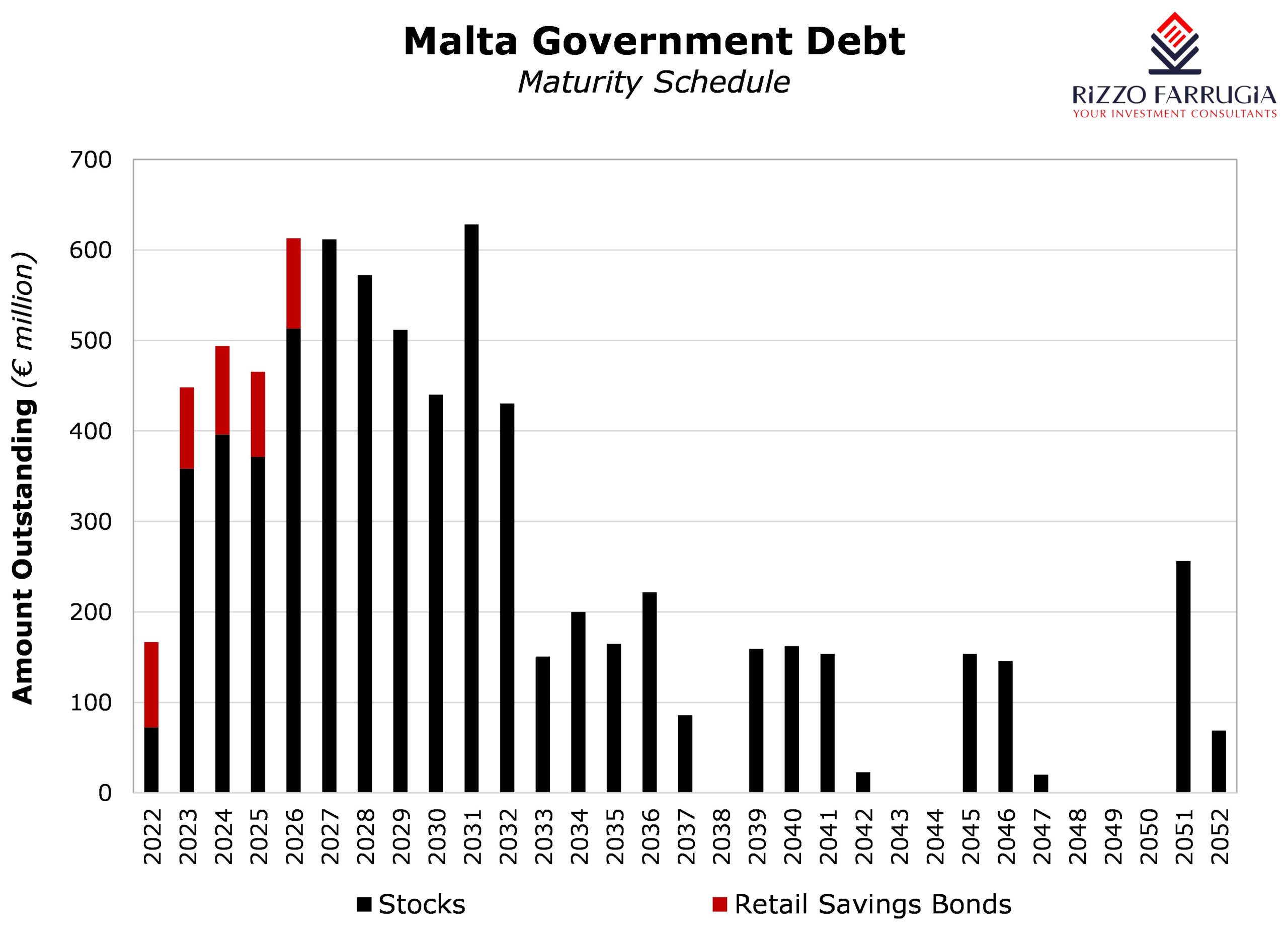

An analysis of the results of the MGS offerings is important in the context of the sharp movements in yields over recent weeks and months as well as the sizeable amount of MGS issuance required in the next few months in order to finance the budget deficit.

In total, the Government of Malta raised €200.6 million (nominal) thereby falling short of the maximum issuance amount of €250 million (nominal).

Subscriptions from retail investors amounted to €57.7 million (nominal) split up as follows: €13.6 million (nominal) in the 2.6% MGS 2028 (V) which is equivalent to 23.6% of the overall retail take-up; €23.3 million (nominal) in the 2.9% MGS 2032 (VI) which is equivalent to 40% of the overall retail take-up; and €20.9 million (nominal) in the 3.4% MGS 2042 (I) which is equivalent to 36.2% of the overall retail take-up.

A total of 2,089 applications were lodged by retail investors translating into an average application amount of €27,600. The most popular among retail investors was the 10-year bond which was priced at a yield-to-maturity of 2.7% per annum followed by the 20-year bond which was priced at a yield of 3.25% per annum. It was not surprising that the least popular by retail investors was the 6-year bond priced at a yield of 2.1% per annum.

The total amount of €57.7 million raised last week represents a significant improvement from the previous retail offerings in June 2021 when only €16 million was raised, and in February 2017 when €19.1 million was raised from retail investors. Potentially, the increased take-up reflects the higher yields offered to retail investors following the sharp upturn over recent months. In fact, the yield on the new 10-year MGS offered last week of 2.7% represents a significant increase compared to the 10-year yield of an MGS of 0.8% at the start of the year and 0.5% at this time last year.

On the other hand, however, one could have also expected the take-up from retail investors to be even larger given the abundance of liquidity across the financial system as was very evident from the demand seen across the multiple corporate bonds successfully issued in recent months. The lack of a more meaningful participation by many retail investors could potentially be due to the psychological impact of the extreme price risk seen in recent months across the MGS market.

In fact, the price of the 1.8% MGS 2051 which was offered to retail investors in June 2021 at 100% (par) declined by an incredible 27 percentage points as the indicative price of the Central Bank of Malta was just below 73% earlier this week. In the same manner, the prices of all other existing MGS also saw sharp declines in prices reflecting the sharp upturn in yields across international bond markets as a result of the very high inflation and the aggressive response by most major central banks to hike interest rates.

From an institutional perspective, just under 75% of the demand was in the 6-year bond as a total of €106.5 million was tendered for, followed by €34.4 million in the 10-year MGS (24.1%) and just a mere €2 million in the longest-dated 20-year offering. The competitive bidding process by the institutional investors highlights some important findings. For example, in the 6-year MGS, the weighted average price of the bids was 102.21% (yield of 2.21%) which is not very different from the fixed price for retail investors at 102.25% (yield of 2.14%). However, there was a large gap between the highest accepted bid at 103.58% (yield of 1.95%) and the lowest accepted bid of 100% (yield of 2.6%). This pricing discrepancy was also very evident in the 10-year MGS with the weighted average price of the bids at only 99.20% (yield of 2.99%) compared to the fixed price of retail investors at 101.75% (yield of 2.7%). Moreover, there was again a very large gap between the highest accepted bid at 102.25% (yield of 2.65%) and the lowest accepted bid of 97.9% (yield of 3.14%). In the previous MGS auction only 2 months ago, the weighted average yield of the 10-year MGS was 1.90%.

The results of last week’s MGS offerings display a challenging environment for the Treasury in view of the required additional issuance of circa €565 million by the end of this year as projected in last year’s budget. This figure excludes further amounts required as the Government has since intervened across a number of industries to provide inflation-related support so as to protect the local economy from significant price hikes evidenced internationally.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.