Banking sector overview

In recent weeks, there were several articles published in the local media explaining the wide-ranging developments currently taking place across the banking sector and also comparing the performances of Malta’s two largest banks during the first half of 2019.

In my view, it would be interesting to also review the performances of the other four core domestic banks, namely APS Bank plc, BNF Bank plc, Lombard Bank Malta plc and MeDirect Bank (Malta) plc.

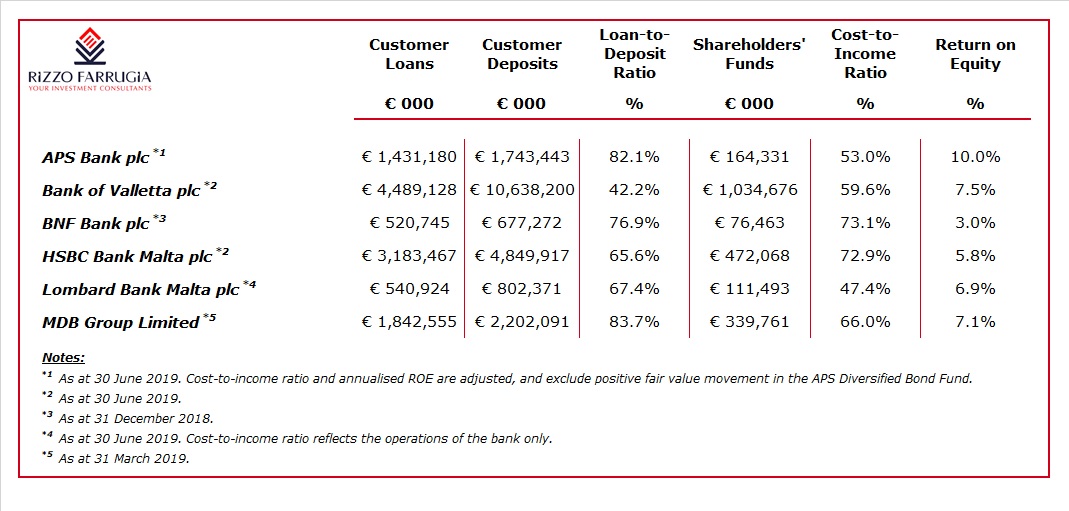

Bank of Valletta plc is by far Malta’s largest bank with total assets exceeding €12.3 billion which is almost double that of HSBC Bank Malta plc. During the first six months of 2019, although BOV’s total income was largely unchanged at just over €127 million, the financial performance of the bank was negatively impacted by a substantial rise in costs as well as the significant loan impairment reversals of €20.2 million recognised in the first half of 2018 which were not repeated this year. In fact, the ‘operating profit before litigation provision’ amounted to €45.1 million compared to the figure of €84.2 million in the first half of 2018. The significant increase in costs due to the start of the bank’s ‘Transformation Programme’ resulted in the cost-to-income ratio deteriorating to 59.6% from 49.1% in 2018. BOV reported a pre-tax profit of €54.3 million compared to the adjusted corresponding figure of €88.5 million in H1 2018 which excludes a litigation provision of €75 million. The net profit generated by BOV in the first six months of 2019 of €38.1 million translates into an annualised return on average equity of 7.5%. The sheer size of BOV when compared to the other banks is reflected in both its loan book and deposit base. Customer loans amounted to €4,489 million as at 30 June 2019 with deposits of €10,638 million resulting in a low loan-to-deposit ratio of 42.2%. Shareholders’ funds as at 30 June 2019 exceeded the €1 billion level which is almost as large as the total amount of equity of the other five core domestic banks put together.

HSBC Bank Malta plc reported a pre-tax profit of €20.9 million in the first half of 2019 which is almost 30% higher than the corresponding figure of €16.2 million in H1 2018. The main factor behind the jump in profitability was due to the significant expected credit loss in 2018 which was not repeated in the first half of 2019. In fact, HSBC Malta benefited from an expected credit release of €1.04 million in the first half of 2019 compared to a charge of €3.36 million in H1 2018. While the main income streams were slightly lower compared to the first half of 2018, HSBC also benefited from a 2.5% decline in total operating costs to €53.6 million with the cost-to-income ratio improving marginally to 73%. Loans and advances to customers increased by €73 million during the first half of the year to €3,183 million while customer deposits declined by €38 million to €4,850 million helping the loan-to-deposit ratio to strengthen to 65.6%. Shareholders’ funds amounted to €472 million with an annualised return on average equity of 5.8%

The consolidated financial statements of Lombard Bank Malta plc include the results of MaltaPost plc and therefore the comparison of certain line items with other banks may be somewhat misleading especially when looking at non-interest income (due to the inclusion of postal sales and revenue) as well as the cost-to-income ratio. Lombard reported a 13.5% increase in net interest income during the first half of 2019 to €10.2 million and an increase in net fees and commissions of almost 24% to €2.62 million. On the other hand, postal sales and other related revenues contracted sharply to €16.4 million compared to €23.7 million. The cost-to-income ratio of the bank on a ‘solo’ basis remained strong at 47.4%. Despite the growth in the bank’s main revenue items, pre-tax profits of the Lombard Group during the first half of 2019 increased by a mere 1.7% to €6.19 million as a result of the higher costs and also the increase in the credit impairment losses to €1.95 million compared to €1 million in the first half of 2018 as the bank aligned its approach to provisioning in line with the requirements of accounting rule IFRS 9. Loans and advances to customers increased by a further €29.8 million during the first half of the year to €540.9 million while customer deposits grew by €14.3 million to €802.4 million helping the loan-to-deposit ratio to improve again to 67.4% from just under 65% as at the end of 2018. Shareholders’ funds increased to €111.5 million which translates into an annualised return on average equity of 6.9%.

The MeDirect Banking Group (MDB) is the third banking institution in Malta falling under the Single Supervisory Mechanism (SSM) together with BOV and HSBC. The SSM refers to the system of banking supervision in Europe comprising the European Central Bank (ECB) and the national supervisory authorities of the participating countries which, in the case, of the MDB Group includes the regulators in both Malta and Belgium. The MDB Group includes MeDirect Bank (Malta) plc and MeDirect Bank SA – a wholly owned subsidiary that handles the group’s operations in Belgium. MeDirect Bank (Malta) does not have its equity listed on the Malta Stock Exchange but has a number of bonds in issue which are listed on the Regulated Main Market with some of these that may be redeemed as from November 2019 with others due for redemption in December 2019. The annual financial statements of the MDB Group as at 31 March 2019 show a profit after tax of €23.3 million. The overall loan book in Malta and also in Belgium stood at €1,843 million as at 31 March 2019 with deposits of €2,202 million giving a loan-to-deposit ratio of almost 84%. Shareholders’ funds as at 31 March 2019 amounted to €339.8 million and the return on equity during their last financial year was 7.1%.

During the first six months of 2019, APS reported that on a consolidated basis, it generated pre-tax profits of €14.9 million which is significantly higher than the €9.3 million generated in the first half of 2018. Although net interest income grew by 13.2% (€2.5 million) to €21.8 million, the main contributor to the strong increase in profitability was from non-interest income which surged to €6.8 million during the first half of 2019 from €2.6 million in the comparative period last year. Similar to the trend seen across the banking sector in recent years, costs incurred by APS continued to spiral higher with a further increase of 13% to €13.9 million. In the press release, APS attributed this to “cost pressures arising from investment in personnel and other operating expenses, including risk and compliance, technology, security and process transformation”. Despite the higher costs, the cost-to-income ratio improved to 48.6% as a result of the significant increase in overall operating income. The balance sheet as at 30 June 2019 indicates that loans and advances to customers (including syndicated facilities) increased by a further €115.7 million during the first half of the year to €1,431 million while customer deposits grew by €93.1 million to €1,743 million. The loan-to-deposit ratio continued to strengthen to 82% indicating that the bank is successfully managing to lend most of its deposits. The condensed financial information published in the press release by APS indicated that shareholders’ funds increased from €140.3 million in December 2018 to €164.3 million as at 30 June 2019. The increase of €24 million in shareholders’ funds resulted from retained earnings arising from profits generated during the period as well as the successful €13 million rights issue in May 2019 which “marked the conclusion of Phase 1 of its Capital Development Plan”. Interestingly the bank stated that “funding strategies may need to be adjusted to optimise spread management”. Despite the increase in the equity base, the annualised return on average equity rose to 14% from just under 10% in the previous financial years which possibly indicates the element of some one-off gains registered during the first half of 2019 which boosted the non-interest income. In fact, APS state that the adjusted return on average equity stood at 10%.

BNF Bank plc did not issue their interim financial statements via a press release. However, some interesting trends are evident from the 2018 financial statements showing net interest income surging from €10.9 million to €15.5 million following the significant growth in customer loans to €520.7 million in December 2018 from €382.3 million at the end of 2017. Customer deposits also increased considerably during 2018 reaching €677.3 million from €513.9 million the previous year with the loan-to-deposit ratio continuing to improve to 76.9%. BNF Bank reported a profit of €2.3 million and a return on equity of 3%.

While the figures portrayed above indicate the ongoing challenging environment for banks which is evident in most countries across the world due to the ever-increasing regulation and the unfavourable interest rate scenario, it is interesting to note the manner in which certain banks realigned themselves whilst others gained market share from the traditional duopoly of the past. In view of the overriding ongoing scenario for banks to maintain higher levels of capital while profitability pressures remain, the return on equity that at times hovered around the 20% level for some of the larger banks before the start of the global financial crisis in 2008, has now dropped to below the 10% level. This is also very much in line with all banks across the eurozone.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.