Hospitality sector battling the pandemic

Since the start of the COVID-19 pandemic during the first quarter of the year, it was clear to all observers that the hospitality sector would be one of the worst-hit industries across the world given the lockdowns and severe travel restrictions adopted by most countries to contain the spreading of the virus.

Despite the easing of restrictions during the early part of summer, the spike in cases across Europe during what normally is the peak of the holiday season resulted in further travel restrictions which dealt a further blow to the hospitality sector. Airline capacity was also further reduced in response to the resurgence of cases and this will result in an extremely challenging period in the months ahead.

On an annual basis I generally pen a few articles on the rankings of companies whose bonds are listed on the Regulated Main Market of the Malta Stock Exchange. Last year I had also published an article specifically on the hotel sector given the increasing number of issuers across this industry. It provided interesting data when comparing some common key performance indicators. In fact, I recall that this was one of the articles that obtained the highest number of views across social media platforms.

The importance of the tourism industry to Malta’s economy is a well-known fact and the large multiplier effect across the entire economy will probably be better understood in these trying times when the tourism sector is almost at a complete standstill.

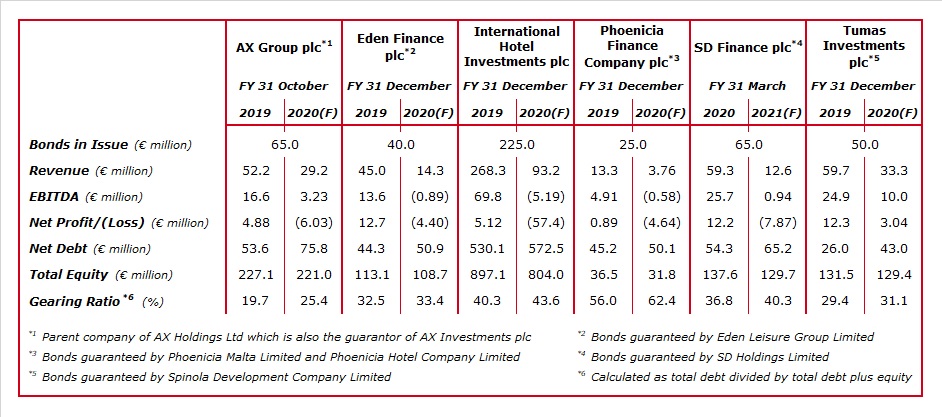

The publication of updated Financial Analysis Summaries by the various bond issuers in Malta was delayed as a result of COVID-19. Following the publication of the last two reports only very recently, today’s article will reproduce some financial figures of the six companies in the hospitality sector whose bonds are listed on the Regulated Main Market of the Malta Stock Exchanged.

While four of the companies have a financial year ending in December, AX Group plc’s financial year comes to an end in October while SD Holdings Ltd (as guarantor of the bonds of SD Finance plc) has a financial year running from April to March. As such, the data provided in the table may not be a perfect comparison given the impact of COVID-19. For example, the forecasts published by AX Group plc for their 2019/20 financial year ending on 31 October 2020 include a total of 4 months (November 2019 – February 2020) before the onset of COVID-19. On the other hand, the forecasts of SD Holdings Ltd cover the financial year from 1 April 2020 to 31 March 2021 and therefore the 2020/21 financial year does not benefit from the boom in tourism pre-COVID.

In fact, as a result of this, the steepest decline in revenue in percentage terms being anticipated from one financial year to the next is of SD Holdings with an expected drop of 79% from €59.3 million in 2019/20 to €12.6 million. As a result of the sharp decline in revenue, SD Holdings is forecasting to report a net loss of €7.87 million compared to the record net profit of over €12 million in the 2019/20 financial year. Despite this loss, the company still expects to have a cash balance of €22.5 million at the end of their current financial year on 31 March 2021. Total debt is expected to increase by 9.5% to €87.7 million following the new €10 million loan taken under the Malta Development Bank COVID-19 Guarantee Scheme.

Although all the hotel operators in their recent announcements and reports mentioned that they embarked on significant cost cutting measures, three of the six companies expect to report negative EBITDA figures during the current financial year (namely the Eden Leisure Group, International Hotel Investments plc and the Phoenicia Group) while SD Holdings is only anticipated to generate an EBITDA of €935,000 compared to €25.7 million in the previous financial year.

The sheer impact of COVID-19 on these hotel operators can be seen from the difference in EBITDA generated from one year to the next. While in the last financial year, these six hotel operators generated over €155 million in EBITDA, it is anticipated that during the current financial year this will drop to a measly €7.5 million.

The most profitable among the six companies is expected to be Spinola Development Company Ltd (as guarantor to Tumas Investments plc) with an EBITDA of just under €10 million. However, one must highlight that this is only due to the fact that the company will be accounting for the final payment of the sale of the building known as the Crystal Ship (adjacent to the Portomaso Business Tower) which will boost the overall performance of the company. In fact, from the report published on 19 August, it emerges that EBITDA from the property development segment of the guarantor is expected to amount to €8.2 million. Moreover, the detailed report reveals that the pure hospitality sector comprising the Hilton Malta hotel is expected to generate an EBITDA of only €65,000 compared to €16.4 million in 2019 as revenue is expected to decline by 68% to €13.2 million.

As advocated in several of my articles over the years, it is important for the investing public to monitor the credit metrics of bond issuers from one year to the next. However, this year, it may be misleading to use the traditional credit metrics such as the interest cover or the net debt to EBITDA to determine the strength of an issuer as a result of such a sharp decline in EBITDA. Naturally, one hopes that the current financial year is not a realistic benchmark and a recovery will begin to show up next year leading to a gradual improvement in cash generation by these hotel operators.

Given the very difficult trading environment for all operators and the resultant difficulty in using EBITDA as a measure of credit worthiness, it remains crucial to monitor the overall indebtedness of the issuer or guarantor to enable investors to try to understand whether shareholder support or additional borrowing would be required for these companies to honour their obligations until their performances begin to improve once tourism numbers start to recover gradually.

The gearing ratio (calculated as total debt divided by total debt plus equity) is therefore an important metric to monitor since it shows the overall financial leverage of the company. The most indebted company among these six hotel operators is the Phoenicia Group with a forecasted gearing ratio of 62.4% given the total debt of €52.8 million and total equity of €31.8 million. On the other hand, AX Group plc has the lowest level of indebtedness with an expected gearing ratio of 25.4% as at the end of their financial year on 31 October 2020.

International Hotel Investments plc has the highest amount of debt in absolute terms forecasted at €622.8 million with a total of €225 million of bonds in issue on the Malta Stock Exchange. This must also be seen in the context of the overall level of equity of over €800 million and the portfolio of properties with a balance sheet value of €1.42 billion as at the end of 2019.

The COVID-19 pandemic brought to an abrupt halt a period of very strong years for the Maltese tourism industry. As most reports by the hotel operators highlighted, various cost cutting measures were implemented in recent months to protect cash flows at a time of significant uncertainty. In the future, it would be interesting to monitor the margins of each of these companies and their individual hotel properties to gauge whether these companies will manage to become more profitable and efficient.

In view of these unprecedented times and the high level of anxiety among many investors, it would be important for these companies, which are among the hardest hit in the pandemic, to issue more regular updates on how their performances are progressing compared to their forecast and whether any other initiatives or funding would be required to ensure that their financial obligations can be duly honoured.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.