Malta Government issues €1.4 billion in stock during 2020

By the end of January every year, the Treasury generally publishes its borrowing plan indicating the projected borrowing requirements of the Government of Malta for that particular year. In January 2020, the Treasury had indicated that the total amount of issuance of Malta Government Stocks (“MGS”) during 2020 was not expected to exceed €450 million since the new bonds being issued were intended to finance the redemption of six MGS issues during 2020 amounting to €461.5 million.

However, as a result of the huge impact on government finances brought about by COVID-19, the Government of Malta resorted to much higher borrowing levels to fund the various initiatives to provide assistance towards targeted sectors of the economy. This is very much in line with developments internationally where most governments resorted to huge levels of additional borrowings to shore up their economies decimated by the pandemic.

Shortly after the onset of COVID-19 and the various measures introduced including the temporary closure of the airport, Malta’s Minister of Finance presented a Bill in Parliament to amend the previous Budget Measures Implementation Act 2020 and increase the borrowing requirement to a maximum of €2 billion.

By the end of the year, the Government issued a total of €1.4 billion in additional debt including the issuance of a further €95 million in 62+ Government Savings Bonds. Apart from the subsidised bonds to pensioners, the Treasury tapped the primary market on 6 separate occasions with the new issuance each time structured via an auction aimed at institutional investors. All the auctions were very well-received with demand abundantly exceeding the available amount on offer on every occasion. The statistics published by the Treasury indicate that local credit institutions were by far the buyers of the large majority of MGS available. This is not surprising given the very high levels of liquidity held by local credit institutions which continued to increase during the pandemic as deposits from retail customers surged. In fact, the latest data provided by the Central Bank of Malta as at the end of June 2020 shows that total deposits held by Maltese residents increased by €826 million during the first half of 2020.

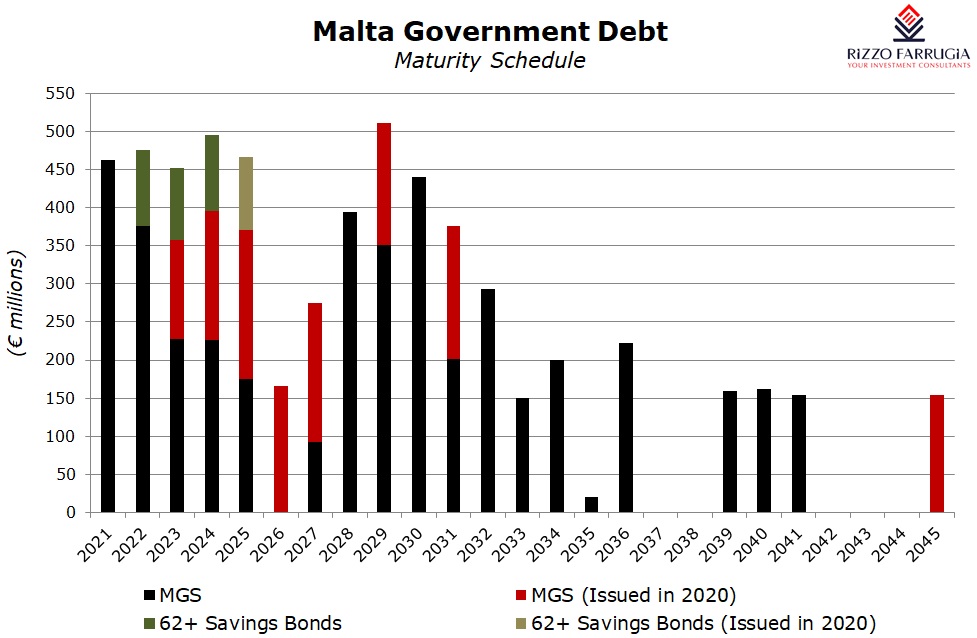

The maturity structure of the various issues that took place during 2020 ranged between 3 years and 9 years with the exception of the first 25-year sovereign bond issue in Malta. In February, the Malta Government issued an MGS maturing in 2045 at a coupon of 1.5% and a further tranche was issued again in November. In total, €153.7 million was issued in the longest-dated security during the year.

An analysis of the overall amounts issued during the year also reveals that between €130 million and €183 million in additional debt was issued in each maturity profile between 2023 and 2027 as well as 2045. This is clearly depicted in the red bars of the graph showing the maturity schedule of the total amount of MGS in issue. The manner in which the amounts were spread across the maturity cycle also enables the government to avoid having an excessive amount of bonds maturing in any single year. Following the additional issuance of €161 million in bonds maturing in 2029, the highest amount now up for maturity is of just over €510 million in 8 years’ time.

Following the record issuance of €1.4 billion in additional government bonds in 2020, the total amount of outstanding MGS and 62+ Savings Bonds is now slightly above €6 billion.

An amount of just over €460 million is due for redemption in 2021. Apart from the need to raise new borrowings to finance these maturities, the Government had already indicated during the 2021 Budget Speech presented to Parliament on 19 October 2020 that the total amount of new borrowing anticipated for 2021 amounts to just under €980 million. It is therefore going to be another busy year for the Treasury to seek to raise this amount during the next 12 months. Hopefully, local credit institutions will maintain a strong appetite to increase their exposure further to Maltese Government bonds to enable the Treasury to successfully raise such amounts.

The financial estimates published as part of the 2021 Budget Speech also indicates that the outstanding amount of MGS is anticipated to continue to rise in the next few years reaching €7.25 billion in 2023.

While this may seem to be an alarmingly high figure, it is worth highlighting that in recent years, Malta’s public finances strengthened materially and its debt to gross domestic product (GDP) ratio dropped to 43% in 2019 which was far below the average across the eurozone economies. Prior to the pandemic, this positive trajectory of a decreasing ratio of debt to GDP was expected to continue with the Government anticipating the ratio to drop to 34.9% in 2022.

However, in view of the sizeable impact of the pandemic on the government finances, the debt to GDP ratio is now expected to increase to just above 60% once again in 2023. Nonetheless, the current historically low interest rate scenario will make it easier for the country to sustain the servicing cost of the new debt issued in 2020. In fact, given the low yields, the additional annual interest payments to service the amount of new MGS issued in 2020 will indeed not be material.

MGS prices had performed strongly during 2019 with a gain of 4.32% in the RF MGS Index (the best performance since 2014) mainly reflecting monetary policy decisions in the euro area as well as other economic and political factors across international sovereign bond markets.

This positive momentum continued at the start of 2020 with the RF MGS Index climbing by a further 1.9% by early March before plummeting almost 6% to 1,094.606 points by mid-June. Thereafter, MGS prices followed a consistent upward trend, but this was not enough for the RF MGS Index to recover all the losses incurred in the first half of the year to end the year with a decline of 0.87%. Trading activity across the MGS market amounted to only €162.9 million across the secondary market compared to much higher levels in previous years. In fact, this level of activity was the lowest since 2006 whilst the average annual level of trading activity between 2007 and 2019 stood at €451 million.

The intense volatility across the MGS market can be explained in the price movements of the longest-dated bond (the 1.5% MGS 2045) which was first issued in February 2020. The price dropped from a weighted-average issue price of 113.22% at the time of the auction in February 2020 to 95% by mid-June. Meanwhile, the weighted-average issue price of the 2045 MGS during the auction in November was 102.68% while at the end of the year, the official price on the secondary market was 118%.

One of the main topics debated during the year was the great disconnect between the indicative MGS prices quoted by the Central Bank of Malta on a daily basis and the prices traded on the secondary market especially for the longer-term securities.

Given the very low yields across the MGS market mirroring the historically low interest rate scenario, very few retail investors are participating in the MGS market except for the 62% Savings Bonds offering subsidised rates to pensioners. The Treasury therefore needs to continue to structure new issuance targeted towards institutional investors.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.