Price Index vs Total Return Index

For several years, investors exposed to the Maltese equity market were accustomed to reading about the performance of the MSE Share Index which was the only index in Malta that tracked the movements of shares listed on the Official List of the Malta Stock Exchange.

However, as from 31 July 2017, the Malta Stock Exchange introduced the MSE Total Return Index.

Some investors may question the motive behind this new index and how the indices differ. Today’s article aims to explain the difference in the methodology used and will also delve into the merits of taking into consideration total returns achieved by investors over the long-term.

The ‘old’ MSE Share Index is a price return index which captures the changes in the prices of the index components. This index ranks companies in terms of their market capitalisation and as such changes in the prices of the larger capitalised companies such as Bank of Valletta plc, HSBC Bank Malta plc, International Hotel Investments plc and GO plc have a much larger influence on the performance of the index than similar percentage price changes in the smaller companies such as Plaza Centres plc.

The most common price return index which is tracked daily by the international financial media is the S&P 500. This is made up of 500 of the largest companies listed in the US and has been in existence in its present format since 1957. On the other hand, the Dow Jones Industrial Average is only made up of 30 companies and the peculiarity of this particular index is that it is not based on the market capitalisation of each of the constituents but it is price weighted. As such, the companies with a higher absolute share price such as Boeing and Goldman Sachs have a much larger weighting than other companies such as Apple and Microsoft although the latter companies are the two largest companies in the index by market capitalisation.

The new MSE Total Return Index is also weighted according to the market capitalisation but it takes into consideration both the price fluctuations of the components of the index (namely all the shares on the Official List of the MSE) as well as dividends that these companies pay. The MSE Total Return Index is based on the assumption that all dividends are reinvested into the index. This is very much in line with the methodology across international financial markets. The S&P 500 also has the total return variant which helps portray the significance and power of dividends and more importantly, the long-term benefits of compounding.

The concept of total returns, encompassing dividend returns and price changes, helps investors understand the long-term benefits of obtaining exposure to equities. Dividend returns form an integral part of the total returns achieved by investors over the long-term and this is very evident from the difference in performance when one compares a price index to a total return index. The S&P 500 in the US for example achieved a cumulative return of 263.5% between 1996 and 2016. However, its total return variant registered a 440.2% uplift during the same period.

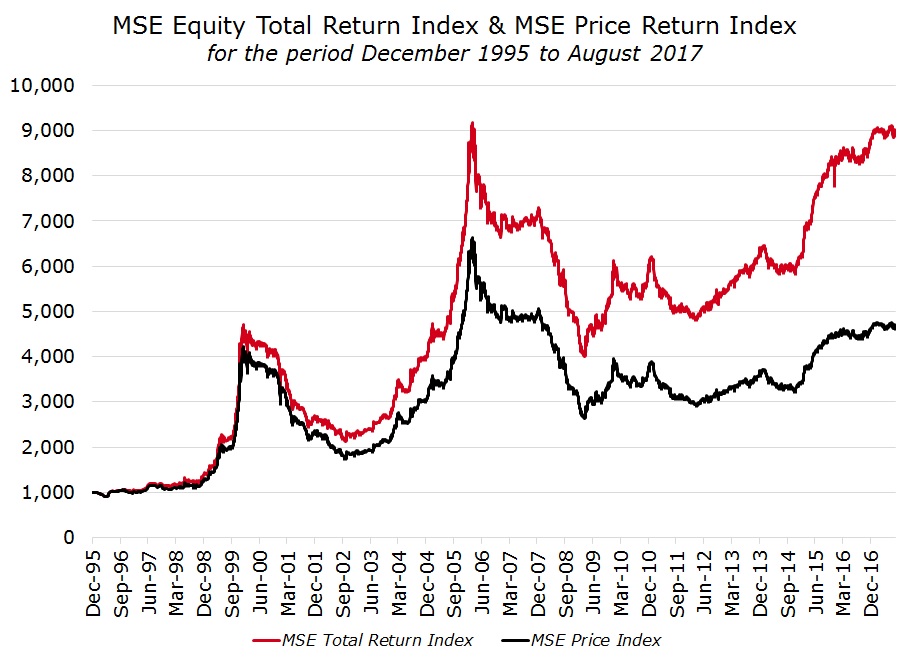

In Malta, this similar pattern also emerged due to the sizeable dividends distributed over the past 20 years. The MSE Share Index shows a total cumulative gain of 363% between January 1996 and December 2016, equivalent to an annual average increase of 7.6%. On the other hand, the MSE Total Return Index shows a cumulative gain of 780% during the same period or an annual average increase of 10.9%.

Dividend paying companies are becoming more popular as a result of the search for yield following the decline in interest rates to historically low levels and the resultant drop in bond yields to levels only marginally above inflation. The yield on a 10-year Malta Government Stock for example declined from circa 4% in mid-September 2012 to a current level of 1.2%. This phenomenon across local and international financial markets has intensified the search for equities offering sustainable dividends and also more attractive yields compared to bonds.

Dividend investing should become a core consideration of an investing strategy for all types of investors irrespective of their age. Naturally, an older investor should allocate a lower percentage of one’s portfolio to equities and dividend paying companies compared to younger investors who can then also have a larger exposure to younger and more speculative companies with higher prospects for capital growth as opposed to the more mature dividend paying companies.

As explained in my article last week, some Maltese companies are holding excess cash on their balance sheets while other companies are underleveraged. These companies are bound to come under pressure from investors to distribute excess cash to shareholders and fund large scale investments via borrowings given the current low interest rate environment. Local investors should therefore continue to monitor these companies since they are likely to be the ones offering sustainable dividends in the years ahead.

On the other hand, bonds have no scope for price appreciation if held to maturity and as such a small exposure to dividend paying companies could be an alternative to beat inflation over the long-term and help investors maintain an adequate standard of living. The loss of purchasing power even with low inflation rates is highly underestimated and very often ignored. International academics have calculated that even if one assumes a relatively low rate of inflation of 2.4% per annum, the value of money halves during a 30-year period. This naturally poses serious problems for pensioners who may not be able to maintain a certain standard of living beyond retirement age due to the overall loss in the value of one’s savings over the years.

In view of these challenges, the power of compounding one’s wealth during a lifetime of savings can have a very positive impact. This is the cornerstone of the investment strategy of value investors such as Warren Buffett. One of his famous quotes is “All there is to investing is picking good stocks at good times and staying with them as long as they remain good companies”. Although Warren Buffett’s Berkshire Hathaway portfolio is a very sizeable one indeed, the large majority of investments are concentrated among a handful of companies which he has held for several years. Coca Cola for example is one of the top holdings within the portfolio of Berkshire Hathaway. It has been calculated that a USD1 investment in Coca Cola shares at the beginning of 1990 was worth USD15.25 by the end of 2015 which is equivalent to an average gain of 11.05% per year including dividends.

Since the MSE Total Return Index is based on the assumption that dividends are reinvested across the index, many investors may question whether this is really achievable. Since most companies in Malta distribute cash dividends, it is indeed very hard to achieve in practice. Furthermore, it is not common at all for investors to reinvest each cash dividend across all the shares listed on the MSE. Some companies however provide the option of a scrip dividend which enables shareholders to increase their exposure to the same company. This method however is generally recommendable for companies who need to increase their equity base and would not be suitable for companies which have excess cash or those companies which are underleveraged.

Despite the difficulty in really achieving what is assumed under a total return index, another concept that still shows the merits of equity investing over a long-term period is the yield on the original investment. This depicts the current return from dividends based on the original cost of an investment rather than the current market value. Many Maltese investors who bought local bank shares in the early 1990’s and have retained these shares until today should be well aware of the significant capital appreciation over the years as well as the very high dividend still being received on the original investment.

The various benefits to all investors from gaining exposure to shares yet again continues to show the urgent need for the Maltese equity market to provide additional opportunities to Maltese investors. The local equity market has not grown as has been expected over the past 25 years. In fact, earlier this year, PG plc conducted a share offering and it was the only equity listing in the past 4 years. Hopefully other companies will consider a listing on the Official List of the MSE and offer shares to the public.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.