Shares vs Bonds

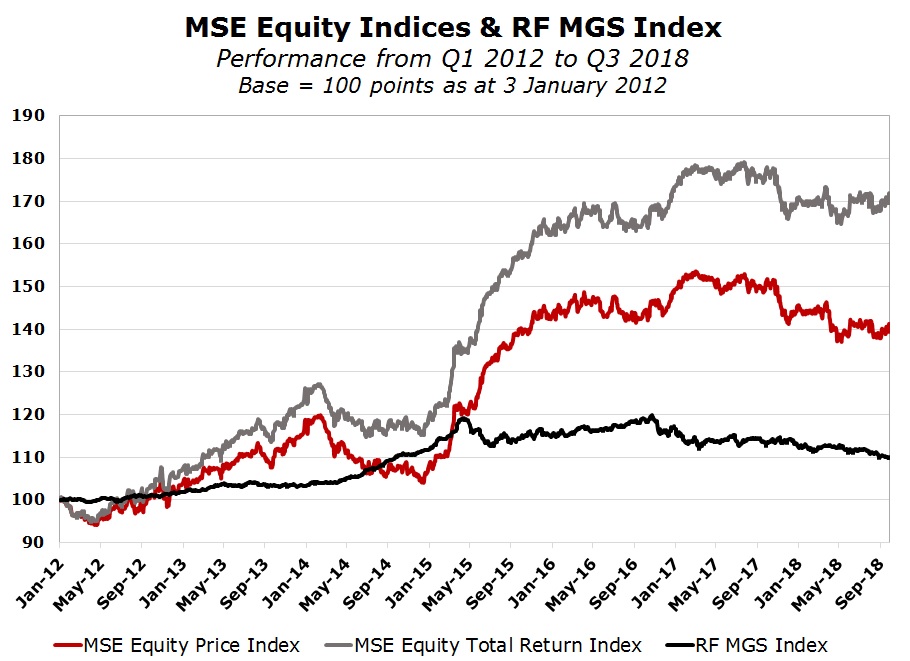

In last week’s article analysing the main movements across the Maltese financial markets during the summer months, I published a graph showing the performance of the two local equity indices compared to the performance of the Malta Government Stock index. This illustration was not limited solely to the past three months but went back to the start of 2012 in order to place the performance of Q3 2018 within the context of the longer term trends across the different asset classes.

The graph, which is being reproduced again today, shows the significant outperformance of shares over MGS during this period. Although it is widely known that shares outperform bonds over the long run, partly reflecting the higher risks associated with investing in equities and despite the higher volatility from one period to another, the extent of the outperformance of equities may be surprising to investors. In fact, the MSE Equity Price Index rose by just over 42% since 2012 (representing a compound annual growth rate [“CAGR”] of 5.4%) while the RF MGS Index advanced by an aggregate 9.2%, representing a CAGR of only 1.3%. Both indices exclude the income generated by shares through dividends as well as the semi-annual interests on MGS.

The Malta Stock Exchange had launched the MSE Total Return Index in July 2017. This not only shows both the price changes across all equities, but also assumes the reinvestment of dividends. Although the MSE Total Return Index was launched in July 2017, data is available also for prior years. Interestingly, the performance of the Total Return Index of +73% since the start of 2012 compared to the growth of 42% in the Equity Price Index clearly indicates the importance of dividends to overall shareholder returns.

The superior performance of the equity market compared to the MGS market must also be seen in the context of the unprecedented monetary policy developments in recent years which naturally impacted very favourably the performance of both asset classes.

Following the global financial crises which commenced in 2008, the world’s major central banks first pushed interest rates down to historically low levels and later also carried out Quantitative Easing programmes. The European Central Bank started its Asset Purchase Programme across the eurozone in early 2015 and this also led to a sharp upturn in MGS prices as eurozone bond yields declined rapidly. The all-time low in the eurozone benchmark yield was recorded on 6 July 2016 when the yield on the 10-year German bund reached -0.204%. MGS prices rallied significantly between 2015 and 2016 leading to some sizeable capital gains for the thousand of investors who were enthusiastically participating in any new issues on the primary market to generate quick returns. The RF MGS Index reached an all-time high almost two years ago when, on 24 October 2016, it stood at 1,182.272 points. Since then the RF MGS Index dropped by 8.4% and it is worth highlighting the considerable declines in the medium and long-term MGS. The steepest decline was registered in the 5.2% MGS 2031 which shed an astonishing 16 percentage points from a price of 155.58% to 139.11%. There were other significant declines also in the 2030 and the 2032 issues. Possibly, few investors who still hold these MGS’s are aware of the steep declines in these MGS prices in only two years.

Although MGS prices plummeted over the past two years, their performance since 2012 can still be considered as exceptional as a result of the boost received from the implementation of the ECB’s QE programme. However, notwithstanding this strong performance, the equity indices still generated superior returns.

Those investors who seek investment advice obtain assistance from financial advisors in order to structure their portfolios in the best manner possible and obtain reasonable exposures to the different asset classes. The optimal allocation is very subjective and it is based not only on the overall investment objectives (income, balanced or growth) but also on a person’s financial situation, age and other considerations. Other investors would opt for discretionary portfolio management leaving the investment decisions firmly in the hands of professional advisors while a large majority of investors still do not resort to professional advice and build up their own portfolio by carrying out execution-only transactions.

The majority of such investors traditionally had a general tendency to obtain a very large exposure in their investment portfolios to fixed-income securities, mainly MGS. Following the recent sharp decline in MGS prices and the superior returns generated by shares over bonds in recent years, such investors should consider whether their portfolios are well structured in the light of the prevailing changes in the interest rate cycle.

The Maltese market has evolved considerably in recent years with several new bond issues being admitted to the Regulated Main Market as well as a handful of new equity issues. Over the past six years, there were Initial Public Offerings by Malita Investments plc, Tigné Mall plc, PG plc and Main Street Complex plc. While 6pm Holdings plc and Crimsonwing plc were delisted, there were the additions of Malta Properties Company plc and Trident Estates plc following the spin-offs from GO plc and Simonds Farsons Cisk plc respectively. Another new equity issuer should be admitted to the Regulated Main Market in the coming months following last week’s announcement by GO plc that it will be seeking shareholder and regulatory approval to conduct an IPO of BMIT Technologies plc. The new names that were admitted to the equity market provided investors with added opportunities to diversify their portfolios not only by seeking higher allocations to the equity market but also by restructuring the equity components of their respective portfolios away from the traditional high exposure to banking equities.

In fact, it is worth highlighting that the outperformance of shares compared to MGS also took place at a time when two of the largest companies on the MSE (namely Bank of Valletta plc and HSBC Bank Malta plc) saw their respective share prices decline substantially, thereby limiting the upturn in the equity indices. For example, BOV is trading at its lowest level in the past six years. The equity indices would have posted far superior returns had BOV’s share price performed positively given its weighting in the overall index.

Although the Maltese equity market has possibly evolved at a slower pace than initially anticipated over 20 years ago, the inclusion of new equity listings in recent years provides investors with a higher degree of diversity with respect to the characteristics of the various companies. For those investors who generally prefer fixed income securities due to their objective of a predetermined level of income, it is worth highlighting that there are a group of locally-listed companies that provide sustainable and regular dividends to shareholders in view of their simple business model and healthy cash generation. These companies, such as Malita Investments plc, Plaza Centres plc, Tigné Mall plc and Main Street Complex plc would best be suited for those investors seeking consistent dividends but with the advantage that dividends may rise over an extended period of time (reflecting a hedge against inflation) apart from the fact that the net asset value of these companies could rise in line with the general trend of the rising value of real estate. The track record of Plaza Centres plc being the company that had first obtained a listing on the MSE in 2000 shows the evident benefits of an exposure to such shares compared to bonds.

The wide movements across the different asset classes over recent years and also the mixed performances across the equity market as was evident in recent weeks with the sharp decline in Bank of Valletta plc compared to the rallies experienced by other equities (namely FIMBank plc, MIDI plc, Malta International Airport plc and GO plc) should instigate many investors to regularly review their portfolios to ensure that these are not only aligned to upcoming macroeconomic developments but also reflect individual company developments.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.