The combined issuance by AX Real Estate plc

The AX Group was one of the first private companies to utilise the local capital markets with a number of its subsidiaries offering financial securities to the public since 1997.

The group has evolved markedly since then and its asset base reached €348 million in 2021. In recent years prior to the pandemic, the financial performance of the group strengthened materially mainly on account of the strong contribution from the hospitality sector which accounted for 73% of overall group turnover in the financial year ended 31 October 2019. Currently, the AX Group has three bonds in issue totalling €65 million which are due for redemption between 2024 and 2029.

In early December 2021, AX Real Estate plc, a fully-owned subsidiary of AX Group plc, obtained regulatory approval for the issuance of (i) 33,333,333 ordinary ‘A’ shares (subject to an over-allotment option of up to a further 16,666,667 ordinary ‘A’ shares) at €0.60 each with a total value of up to €30 million and (ii) €40 million in unsecured bonds at a coupon of 3.5% and redeemable in 2032.

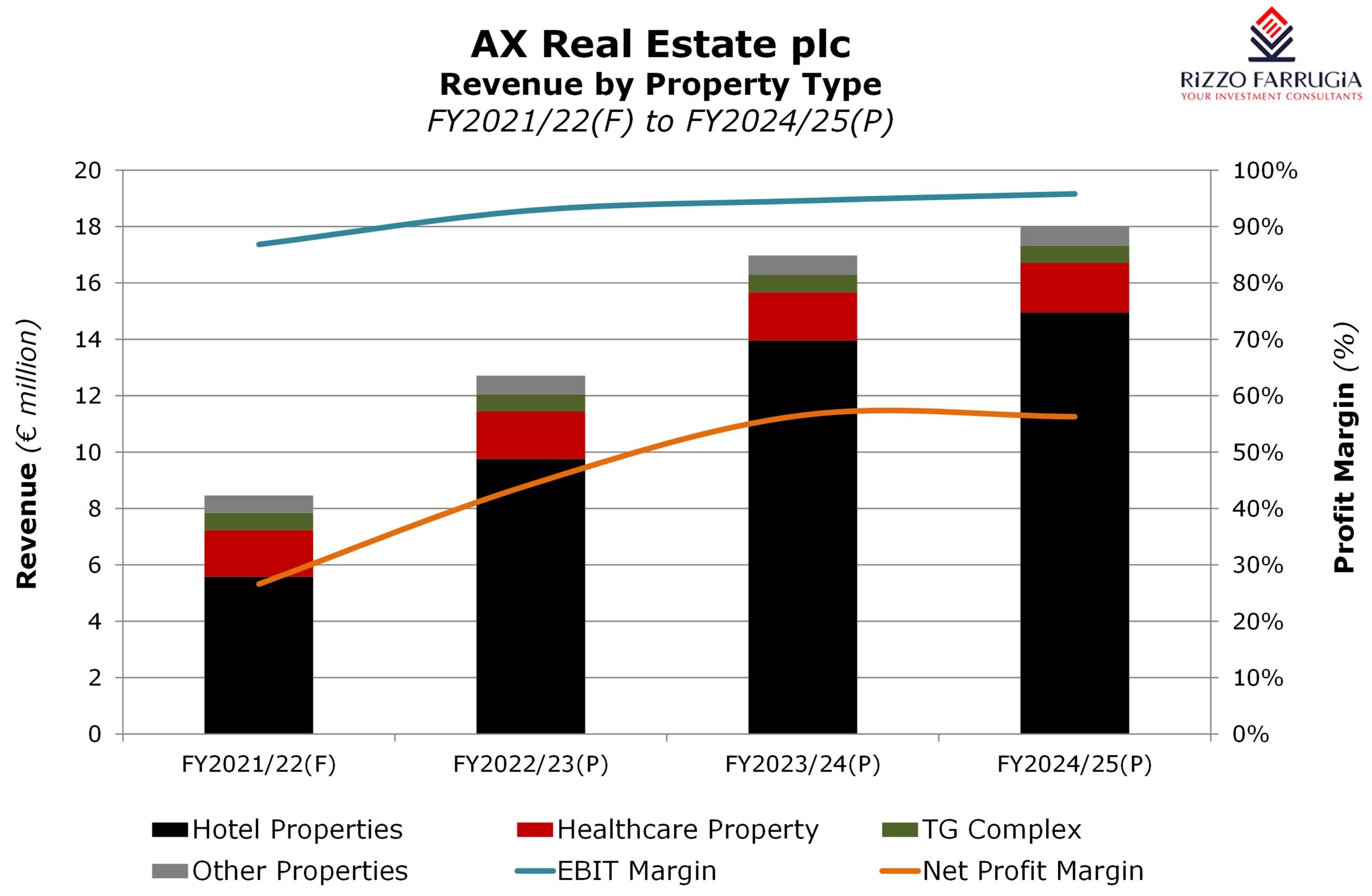

AX Real Estate owns a diversified portfolio of properties which are mainly leased for the long term to the parent company AX Group plc. The properties have a total value of just over €230 million and comprise hotels and adjoining leisure/catering facilities and serviced apartments (valued at €170.9 million and representing 74% of the total value of the property portfolio of AX Real Estate); a healthcare and retirement complex (valued at €36.9 million); residential and commercial units as well as office space (valued at €16.4 million); and industrial property that comprise nine warehouses and an adjoining office block (valued at €6.95 million). The lease agreements typically include a minimum pre-set base rent, and in the case of the hotel properties, an additional variable component is dependent on revenue targets capped at a fixed percentage of the hotels’ gross operating profit.

The new capital and debt issuance by AX Real Estate is required in order to finance two key development projects – the redevelopment and extension of the Seashells Resort and the development of the Verdala Hotel. Permits were obtained in 2021 and these projects are expected to be a major driver of the company’s future growth in the next few years.

The redevelopment and extension of the Seashells Resort represents the first phase of the master plan for upgrading the company’s foreshore properties in Qawra. The initial investment of around €52 million will add four new floors to the Seashells Resort. As a result, the hotel’s total number of rooms will increase by 166 to 618 rooms whilst there will also be the complete renovation of the property’s facilities such as pools, restaurants, and bars. In addition, the lido at the Seashells Resort will be demolished and redeveloped subject to the relevant permits being obtained from planning authorities anticipated during Q1 2022. Works on ‘Phase 1’ of the master plan commenced in November 2021 and are expected to be completed by April 2023.

The Verdala project entails the demolition of the former Grand Hotel Verdala and the construction of a new five-star 25-suite luxurious hotel. In addition, the existing 19 apartments that will lie adjacent to the hotel will be completely refurbished to the high level of finishings at par with the hotel. Works started in August 2021 and the entire project, which is estimated to cost €11.5 million, is expected to be completed by the end of 2023.

Although AX Real Estate is a relatively new company having only been established in June 2019, its main operating assets have been in existence for several years. The company’s profitability is expected to be continued to be dampened at least until FY2023/24 in view of the projected gradual recovery in tourism as well as the completion of the two major projects which the company is currently pursuing.

As such, FY2024/25 represents the benchmark year for AX Real Estate as it will include the initial twelve-month contributions from the enlarged and completely renovated Seashells Resort and the new Verdala Hotel as well as the anticipated impact of the full recovery in tourism.

In this respect, it is important to highlight that around 78% of the projected revenues to be generated in FY2024/25 are based on pre-set minimum fixed rents and only the remaining portion of 22% (amounting to €4 million) is dependent on the hotels’ performances. In either case, it is envisaged that the hotel properties will always represent the majority of the income generated by AX Real Estate even when excluding the variable top-up rents based on the hotels’ performances. The Prospectus reveals that revenues are expected to reach €18 million by FY2024/25 which translates into a gross rental yield of 6.3% on the value of €286.1 million of investment property.

AX Real Estate aims to distribute the majority of its yearly distributable profits provided that it maintains a minimum cash reserve of €1 million. The company is committed to a minimum net dividend yield of 4% in respect of the financial years ending 31 October 2022 and 2023. Thereafter, following the completion of the Qawra and Verdala projects, the company is forecasting higher dividend yields which rise to 5.07% for FY 2024/25. Such dividends are however dependent on, amongst other factors, its profitability, debt servicing and repayments, cash flows, working capital requirements and investment commitments, as well as the prevailing market outlook at the time.

Applicants are required to apply for a combination of shares (minimum application of 5,000 shares equivalent to €3,000) and bonds (minimum application of €2,000 nominal) in order to be considered for any allocation of bonds unless an investor applies solely for a minimum of €250,000 in bonds.

Beyond the Verdala and the Seashells Resort projects, AX Real Estate has other investment plans for the future. These consist of ‘Phase 2’ of the Qawra master plan which will centre around the redevelopment of the Sunny Coast Resort into a new 200-unit aparthotel and the extension of the Hilltop Gardens Retirement Village. The retirement village currently has an inventory of 133 residential units which are presently all leased out for the long-term. AX Real Estate is currently in the process of obtaining the necessary planning approvals for the construction of an additional 50 residential units across two new floors which will be earmarked for lease in line with the existing business model of the Hilltop Gardens Retirement Village. The financial projections in the Prospectus covering the financial year until 2024/25 do not capture the potential additional value and incremental profits that should emanate from the extension of the Hilltop Gardens Retirement Village and ‘Phase 2’ of the Qawra master plan.

The addition of AX Real Estate to the local equity market would mark an important step for the continued evolution of the AX Group over the years as it transitions away from its private ownership structure by accepting public share ownership. Such a move is fundamental for the continued growth of the wider group given its ambitions going forward and the overall size of its upcoming investments.

Rizzo, Farrugia & Co. (Stockbrokers) Ltd is acting as Joint Sponsor to AX Real Estate plc.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.