The return of the euro

In last week’s article, I explained the impact on the international and local bond markets from recent monetary policy statements as well as political developments in the US. Naturally, these events also influenced the currency markets.

As a start, it is worth recalling that currencies are valued against one another and therefore the performance of a currency signifies relative strength or weakness against another currency. The two most common exchange rates tracked by Maltese investors is the EUR vs USD and the EUR vs GBP. As such, movements of the EUR vs USD exchange rate are dependent on political and economic factors in Europe and also the US while movements in the value of Sterling against the euro are dependent on factors affecting the UK economy as well as developments across the Eurozone.

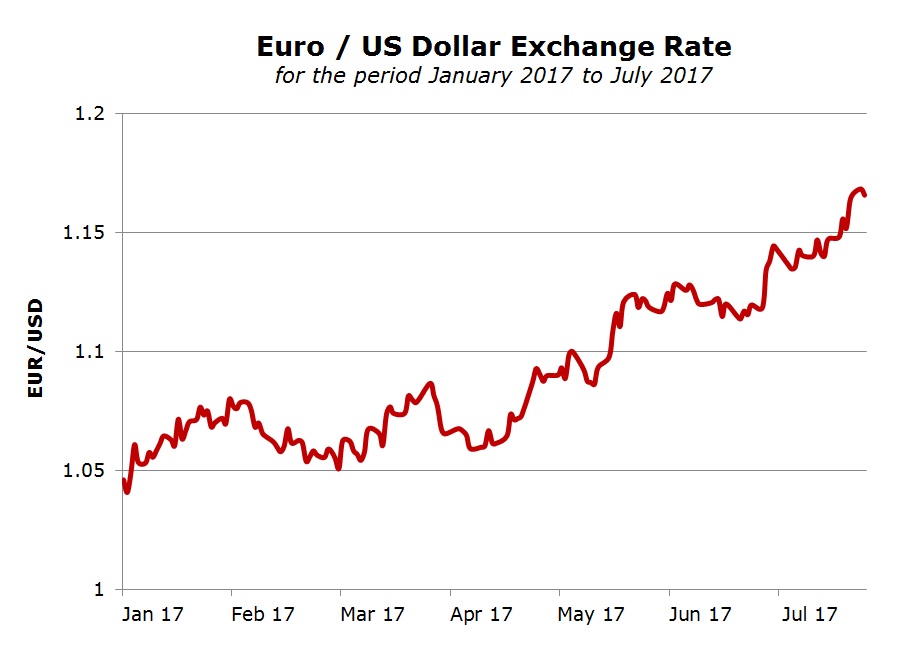

Within this context, the increase in the value of the euro against the US Dollar in 2017 has been remarkable. The euro had been strengthening against the US Dollar in recent months due to the economic recovery across the Eurozone, the timing of the anticipated reduction of the quantitative easing programme by the European Central Bank (ECB), heightened political uncertainty in the US as well as occasional comments by the US President Donald Trump that the value of the US Dollar is too high against the euro which in turn hurts American exporters. The single currency had traded up to a level of USD1.15 just prior to the ECB monetary policy meeting held last Thursday 20 July 2017, representing a gain of over 11% from the 2017 low of USD1.0339 touched on 3 January 2017.

The ECB’s monetary policy meeting which was held last Thursday was another key event for bond as well as currency markets. The ECB left its monetary policy unchanged and it also maintained the possibility of increasing its monthly purchases of assets. The ECB also noted that its current quantitative-easing programme of €60 billion per month will continue until the end of December 2017 “or beyond, if necessary” amid concerns that a tighter monetary policy could endanger the economic revival of the single currency area. Furthermore, the ECB added that it “continues to expect the key ECB interest rates to remain at present or lower levels for an extended period of time, and well past the horizon of the net asset purchases.”

The President of the ECB Mario Draghi also commented that the central bank’s Governing Council will discuss the future of its quantitative-easing programme later this year. Many international financial analysts expect an announcement of the reduction in the QE programme (commonly referred to as ‘bond tapering’) in September or October with some speculating that the purchase programme will be reduced to €40 billion per month as from January 2018 and then completely phased out by the middle of 2018. By then, the ECB would have reportedly exhausted the available amount of bonds that it may purchase under current rules for many countries including Germany. Should the ECB stick to the statement by Mr Draghi that interest rates will remain at present levels until well past the timing of the purchase programme, this would imply that no interest rate hikes will take place until 2019.

Despite the cautious comments by the head of the ECB, the euro strengthened further and last Friday it reached a fresh two-year high against the US Dollar of USD1.1684.

Currency traders were on the lookout to see whether the President of the ECB would indicate that the strengthening euro posed a risk to the economic recovery across the Eurozone. In response to a specific question by a journalist following the ECB meeting, Mr Draghi failed to quash the recent rise in the euro. Many interpreted the lack of reference to the appreciation of the euro as an indication that the ECB appears at ease with the euro strength and does not seem very concerned about the market reaction so far.

Last week’s renewed rally in the euro was therefore in anticipation of the tapering of the bond buying programme in the months ahead and also as a result of the lack of comments by the ECB President against the risks of a rising currency.

The strengthening of the euro to a fresh 2-year high against the US Dollar took its toll on European equity markets. A stronger currency makes exports less competitive as they become relatively more expensive for overseas buyers while a weaker currency generally boosts earnings from overseas. The German economy is the largest one in the Eurozone which is highly reliant on exports. As such, the upturn in the value of the euro negatively impacted the German stock market with the DAX 30 hitting a 3-month low of 12,142 points on Monday 24 July from its all-time high of just under 13,000 points recorded on 20 June 2017, representing a decline of just over 6%, thereby trimming the year-to-date gains to around 6%.

Other European bourses also faced selling pressure in recent weeks. Similar to the DAX 30, the French CAC 40 also dropped to a fresh 3-month low of 5,094.36 points on Monday 24 July, representing a drop of over 6% from its 2017 high of 5,442.10 points registered on 8 May. Another widely quoted index is the Euro Stoxx 50 which represents a basket of blue-chip European companies which are leaders in their respective fields. Similar to the DAX 30 and the CAC 40, the Euro Stoxx 50 also recorded a 3-month low of 3,431.19 points last Monday, again representing a decline of over 6% from its 2017 high of 3,666.80 reached on 8 May.

Against this background, it is also very interesting to note that during the 11-week period between 8 May and 24 July, the Euro-US Dollar exchange rate strengthened to 1.1639 from 1.0924, representing a gain of 6.5%.

Two sectors very much reliant on exports – industrial groups and producers of consumer discretionary goods – were among the major losers last week. For instance, the equities of three large export-oriented European multinationals – Sanofi (a French company which is also one of the largest pharmaceutical companies in the world), Siemens (a global conglomerate particularly renowned for the provision of heavy industrial solutions) and BASF (the largest chemical producer in the world) – dropped by more than 3%. Likewise, the equity of Volkswagen – which is the largest automaker in the world in terms of number of cars sold – lost 3.6% whilst the share prices of the top two European luxury-car makers BMW and Daimler dropped by over 3%. The shares prices of these three auto companies extended their declines last Monday on reports suggesting that the European Commission was assessing information on the alleged collusion between Volkswagen, BMW and Daimler in running secret technology working groups together. In this respect, whilst the European Commission affirmed that it still “premature at this stage to speculate further”, BMW categorically denied the allegations.

Last year, many international analysts were of the view that the euro will weaken and reach parity (1:1) against the USD. This not only did not materialise but the euro has strengthened by over 11%% this year and by nearly 13% from its low of USD1.0339 in January. Meanwhile, following the recent events as documented above, coupled with the growing political uncertainty in the US, some economists now believe that the euro can continue strengthening and may reach USD1.20 by the end of 2017.

Maltese investors with high exposures to the US Dollar in their portfolios would be negatively impacted by recent developments. In addition, local companies earning a good portion of their respective revenues in US Dollar might also be at risk of being impacted negatively when translating their financial results into euro – their reporting currency. By way of example, following the acquisition of the METS Group early in 2016, Medserv plc generated 40% of its total revenues in USD. As many investors have experienced over the years, currency markets can also be rather volatile and lead to wide fluctuations in investment portfolios. Investors must therefore ensure that the currency mix in their portfolios also reflects their over-riding objectives.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.