PTL expects lower profits as export business terminated

PTL Holdings plc, a subsidiary of Hili Ventures Limited, published its updated Financial Analysis Summary (FAS) on 21 August. Since the FAS was published after 1 July, PTL was not only obliged to update its forecasts for 2015 but was also required to provide its projections for 2016.

PTL Holdings was established in 2013 and acts as a holding company and financing arm of three IT companies which were acquired by Hili Ventures recently. Initially, PTL Limited (formerly Philip Toledo Ltd) was acquired in 2012 and two larger acquisitions took place in 2014 – SAD in June 2014 for €40.35 million and APCO in August 2014 for €8.8 million.

Although the Prospectus published at the time of the bond issue of PTL Holdings in November 2014 provided financial statements for 2013 and 2014, these were drawn up on a ‘pro-forma basis’ and were useful for illustrative purposes only since they assumed that PTL Holdings had control over both SAD and APCO during the review period.

As such, the 2014 audited financial statements of PTL Holdings published on 30 April 2015 should not be compared to the figures found in the Prospectus.

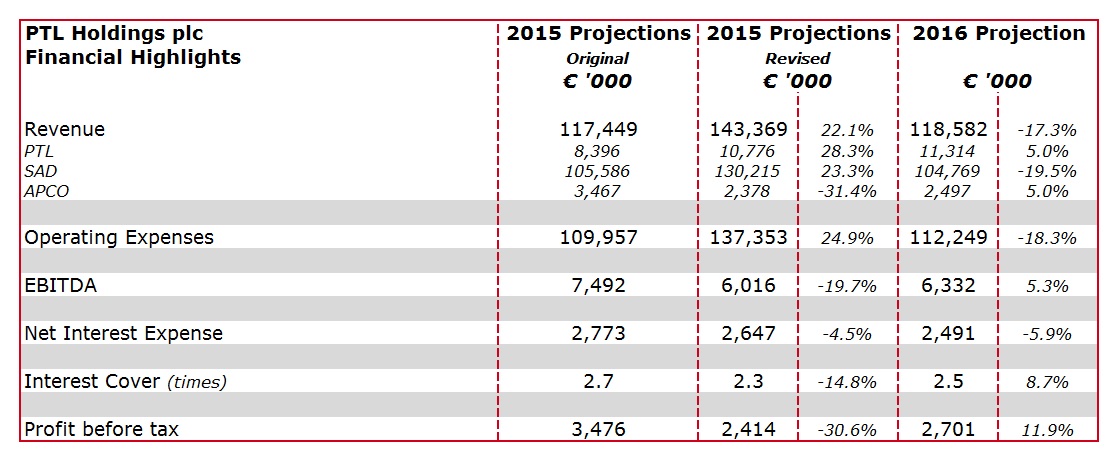

On the other hand, however, one can compare the 2015 projections published in November 2014 to the FAS update of a few weeks ago. In November 2014, PTL had expected revenue to amount to €117.4 million during 2015 and they now expect this to rise to €143.4 million. Notwithstanding the 22% additional revenue for 2015, PTL expect to generate earnings before interest, tax, depreciation and amortisation (EBITDA) of only €6 million which is 20% below the figure of €7.5 million projected in November 2014. In fact, the 2015 EBITDA margin is expected to shrink to 4.2% compared to the earlier expectations of 6.4%.

Unfortunately the FAS does not provide a justification for this wide variance. This would have been useful information for the many investors who invested in PTL bonds during the primary market offering in November 2014 as well as those who continued to support this bond despite the rally in the bond price on the secondary market to above 111%.

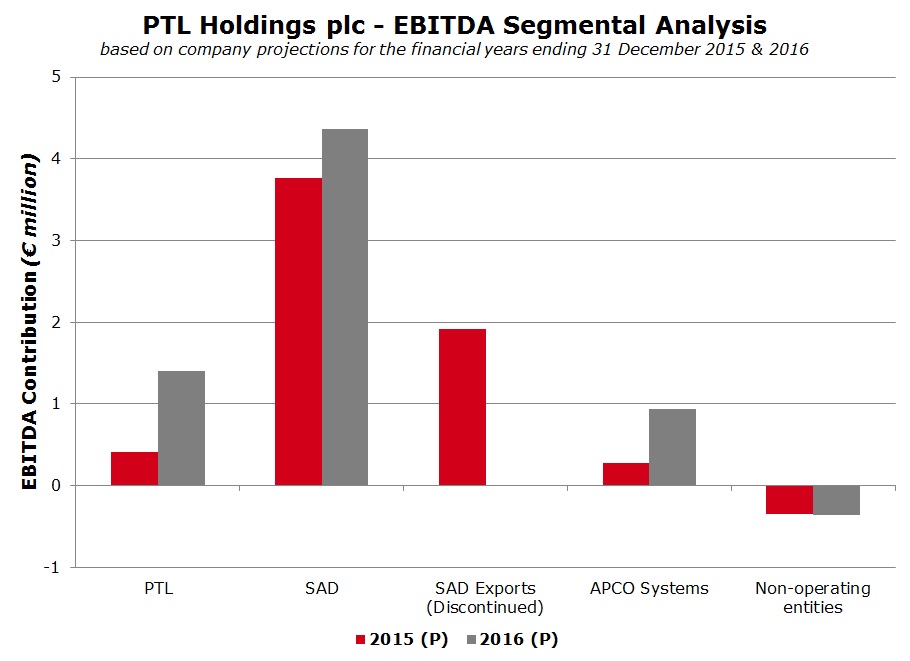

One of the major reasons for the expected dilution in EBITDA could be due to the termination of the SAD export business comprising the distribution of electronic goods across a number of European countries. In the 2015 interim financial statements, it was disclosed that this business was being discontinued due to a change in VAT regulations and the risks associated with cross border sales of technology items. During the first few months of 2015, this line of business generated total revenue of €34.8 million. The updated FAS provides the EBITDA breakdown across the different business units for both 2015 and 2016. The EBITDA contribution of the SAD export business during the first few months of 2015 was €1.9 million, representing a margin of 5.5%.

Meanwhile, the core business of SAD, comprising the resale of Apple products through the various iSpot outlets across Poland together with the business-to-business offering, is expected to generate €95.4 million in revenue in 2015 and EBITDA of €3.8 million giving a margin of only 3.9%. The contribution from PTL Limited and APCO is expected to be minimal in 2015 with EBITDA of €0.4 million and €0.3 million respectively.

However, the Directors expect the EBITDA of both PTL Ltd and APCO to rise significantly in 2016 despite a minor improvement in revenue generation. The EBITDA of PTL Ltd is expected to jump to €1.4 million in 2016 from only €0.4 million in 2015 (with the EBITDA margin rising to 12.4% from 3.8% in 2015) and APCO’s EBITDA is anticipated to reach €0.9 million in 2016 from €0.3 million in 2015 (with the EBITDA margin surging to 37.4% from 11.4% in 2015). The FAS does not explain the assumptions behind the significant improvement expected by both PTL Ltd and APCO in 2016. Should PTL Ltd and APCO succeed in achieving this projected growth, the contribution of these two entities to overall EBITDA of PTL Holdings will improve from 11.3% in 2015 to 37% in 2016. Furthermore, SAD’s revenue is expected to grow by 9.8% in 2016 to €104.8 million and EBITDA to rise by 15.8% to €4.4 million with the EBITDA margin edging up to 4.2% from 3.9% in 2015.

Despite the expected improvement from PTL Ltd and APCO, PTL Holdings remains highly dependent on SAD to generate sufficient cash to cover its interest payment obligations and the repayment of the bonds upon maturity. As such, a lot depends on the Apple brand and SAD’s ability to maintain its non-exclusive franchise agreement with Apple Inc.

The more important ratios for bond investors to follow from one review period to the next are the interest cover and the gearing ratio. Notwithstanding the weaker-than-expected EBITDA contribution in 2015 compared to the original forecasts, the interest cover is still anticipated to amount to 2.3 times in 2015 and this is expected to improve to 2.5 times in 2016. On the other hand, however, PTL Holdings remains one of the most highly leveraged companies among the bond issuers on the Malta Stock Exchange. The gearing ratio forecasted as at the end of the current financial year is expected to remain above 86%, represented by shareholders’ funds in excess of €7 million and total debt of almost €45 million.

The Financial Analysis Summary has once again proved to be a useful document to enable investors to monitor the performance of bond issuers. However, such companies should also convene meetings with financial analysts to discuss industry trends and to provide more in-depth explanation on the financial statements, including the variances within the forecasts. This would greatly assist investors in their decision-making process.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.