What has contributed to recent Sterling weakness?

Many Maltese investors who have exposure to the British pound as part of their overall investment portfolios may have noticed a sizeable decline in the value of Sterling against the euro over recent months.

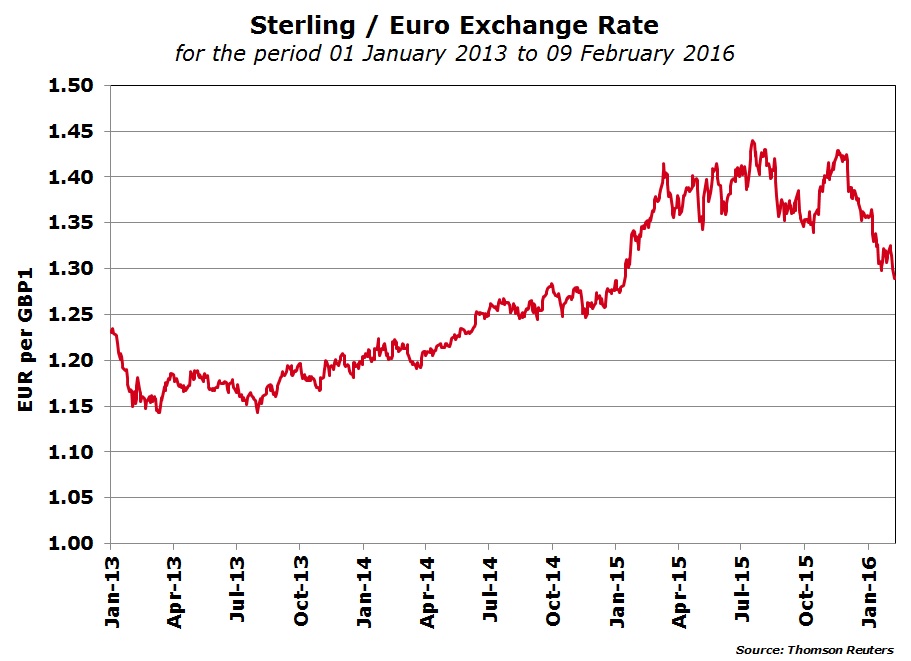

The bull run since early 2009 from close to parity versus the euro was halted six months ago when, in mid-July 2015, the exchange rate reached a high of EUR1.4399 for every GBP1 (or GBP0.6945 per EUR1). After a brief downturn over the summer months, it then re-tested its multi-year highs in November but since then the value of the British Pound slumped by over 10% to the EUR1.289 level (equivalent to GBP0.7758).

Given the importance of the performance of Sterling for Maltese investors as well as business owners and consumers in general, it is worth analysing the reasons for such a downturn in a relative short period of time.

Currencies are valued against one another and therefore the performance of a currency signifies relative strength or weakness against another currency. In this case, the movement of the Sterling vs Euro exchange rate is dependent on factors affecting the UK economy as well as developments across the Eurozone.

The main influential factors which contributed to the recent volatility in the value of Sterling are the performance of the British economy and expectations on the future direction of interest rates, as well as the uncertainty surrounding Britain’s membership of the EU.

On the economic front, the Governor of the Bank of England (BOE) Mark Carney has played a central role in affecting currency movements. In the summer months, he had signalled that the decision to raise interest rates which have been on hold at historic lows since March 2009, might come into focus “around the turn of the year”. With the market widely anticipating the start of tighter monetary policy in Britain similar to the US, sterling reversed its downward trend and strengthened once again until mid-November.

However, the Governor of the BOE backtracked somewhat over recent months as plunging oil prices and slowing global growth stemming from a deteriorating Chinese economy are weighing on inflation expectations across the UK. This began to lead to the decline in the value of Sterling.

In its latest monetary policy meeting held last week, the BOE cut its forecasts for economic growth, inflation and wages due to “sustained financial market turbulence”. Mr Carney stated that “global growth has slowed again over the past few months, as emerging economies decelerated and the US economy grew less than expected”.

The UK economy is now expected to grow by 2.2% this year, from a projected 2.5% in November. Economic growth in 2017 is expected to be 2.4% compared to an earlier forecast of 2.7%.

The BOE now expects an average inflation rate of only 0.8% this year climbing to the 2% target in 2018.

While the BOE seemed to signal that interest rates would now remain on hold until next year, some economists are expecting the first rate hike in August 2018 while others have gone as far as forecasting that there will be no rate hikes until the end of the decade (i.e. 2020). Such anticipations from these economists is what led to a further weakening of sterling against the euro since last week.

Central banks all over the world are deliberating how to handle slowing consumer prices. The US Federal Reserve has signalled it may delay a further rate hike which was anticipated to happen next month while the European Central Bank is widely considering fresh stimulus at its next meeting on 10 March. Moreover, since the recent surprise decision by the Bank of Japan to push interest rates into negative territory, there was speculation that the BOE would also consider such a move. However, at last week’s monetary policy meeting, BOE officials quashed talks of a rate cut in the near term as they argued that keeping inflation within their target would require tighter monetary policy (i.e. higher interest rates) over the next three years.

However, Mr Carney stated that the BOE “stands ready to take whatever action is needed, as events unfold, to ensure inflation remains likely to return to target in a timely fashion”. In his letter to the Chancellor of the Exchequer George Osborne, he also said that should “downside risks materialise, market expectations of the future path of interest rates could adjust further to reflect an even more gradual and limited path for bank rate rises than is currently priced”. The value of the British pound will remain very sensitive to such statements until such time as the future direction of interest rates becomes clearer.

In addition to the global headwinds and the impact on the British economy, the other important factor affecting the value of sterling is Britain’s upcoming vote on EU membership. Although upon being re-elected in May 2015, Prime Minister David Cameron vowed to hold a referendum by the end of 2017, this is now likely to take place by summer 2016. So far the Government has not yet managed to conclude a deal with the EU although this is possible by the end of February. If the British people were to vote to exit the EU, a new form of trading relationship with the EU would need to be found. The uncertainty over what this relationship would be, and the length of time to reach a final deal, could lead to heightened uncertainty and which will negatively impact the value of Sterling. The US investment bank Goldman Sachs claims that the British pound could crash by 20% if the UK votes to leave the EU. Another US financial institution, CitiGroup, warned that “the effects of Brexit, if it happens, are likely to be large and painful in economic and political terms, both for the UK and the overall EU”.

Movements in sterling should be of interest to various operators in different sectors of the local economy. Among the most important, a weakening of sterling is not necessarily good news for tourism operators including the local hotel industry. The UK market remains the largest source market for Malta and a weakening currency makes a holiday to an EU destination more costly for British travelers. However, thankfully, this does not seem to be having an effect on Malta as recent statistics continue to indicate an increase in overall tourism numbers including from the British market.

On the other hand, a weakening sterling may be beneficial for other sectors of the economy. The first that comes to mind is car importation, more specifically related to second hand vehicles from the UK. The recent weakness of sterling is good news for such operators as British imports will be more competitive and local consumers will be more prone to favour a second hand British import. Importers of other merchandise from the UK including foodstuffs would very much welcome the recent decline in the value of the British pound.

Notwithstanding the recent downward trend, continued volatility in currency markets is likely to persist especially in the coming months ahead of the referendum. Apart from the factors impacting the British economy including the very important referendum, news from the ECB will continue to impinge in a significant way on the value of the euro against all major currencies including Sterling. Wide movements in currency markets has numerous implications for investors, businesses and consumers and hence the need to continuously monitor developments and to take appropriate action in a timely manner.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.