Opportunity cost of holding excess liquidity

In October 2022 I had published an article explaining the concept of the Treasury Bill market with specific reference to the surge in issuance in view of the sudden rise in interest rates which made these securities more appealing to the investing public most especially for companies in their treasury management activities.

Treasury Bills, or T-Bills, are short-term financial instruments issued by Governments worldwide with maturities of up to one year. T-Bills are referred to as ‘zero-coupon’ bonds. Maturities can be for 1 month, 3 months, 6 months, 9 months or 1 year although the 3-month and 6-month T-bills are the ones most commonly issued.

In Malta, T-Bills are issued every week through a competitive bidding process (auction). The auction is typically held every Tuesday and the Treasury publishes a calendar every month giving advance notice of the issuance on a weekly basis.

Treasury bills are issued at a discount and are redeemed at face value. The difference between the purchase price and the par value is the interest earned for holding the T-Bill for a specific period of time.

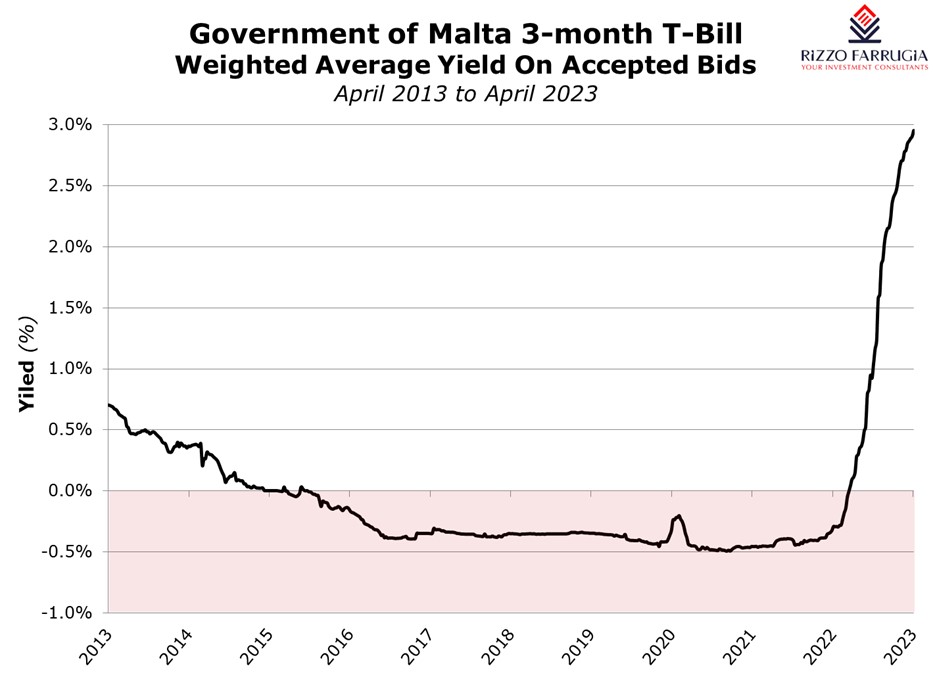

In line with the upward movements in yields worldwide, the Malta Government Treasury Bills also experienced a sharp upswing in yields over recent months.

An analysis of the tenders across the T-Bill market indicates that the weighted average yield of the 3-month T-Bill has jumped towards the 3% level in recent weeks compared to negative yields until June 2022 and a yield of below 1% until the first week of October 2022. The 3-month T-bill was producing a negative yield from May 2015 to June 2022 before surging in the past nine months in line with the 3-month Euribor which is an important benchmark since it is the interest rate at which a selection of European banks lend funds to one another.

A similar pattern occurred in the yield of the 6-month T-Bill. The weighted average yield of the 6-month T-Bill increased to the 3% level in recent weeks compared to negative yields until June 2022 and a yield of below 1% until the end of August 2022. The 6-month T-bill was producing a negative yield from November 2015 to June 2022.

However, it is worth noting some interesting movements in yields during the past two auctions. Last week, the cut-off rate of accepted tenders in the 3-month T-Bill at 2.95% was marginally above the cut-off rate of accepted tenders in the 6-month T-Bill at 2.947%. On a weighted average basis, however, the yield on the 3-month T-Bill of the accepted bids was 2.905% which was minimally below the 2.91% of the 6-month T-Bill.

Meanwhile during this week’s auction, the cut-off rate of accepted tenders in the 3-month T-Bill surpassed the 3% level for the first time in a long number of years. Moreover, this exceeded the yield of the cut-off rate of accepted tenders in the 6-month T-Bill at 2.95%. On a weighted average basis, the yield on the 3-month T-Bill of the accepted bids this week was 2.953% which is above the 2.944% of the 6-month T-Bill.

In view of the significant upward movement in yields, there is an evident mobilisation of liquidity which was lying idle in the banking system into other instruments offering superior returns across the financial markets.

Although this was reflected in the steady demand across the local corporate bond market over the past several years, this became more evident over recent months especially when the Treasury issued 10-year Malta Government Stocks in October 2022 at a rate of 4% per annum. Retail investors reacted very positively to this offering with just under €300 million taken up within a few days thereby crowding out the institutional auction. In the most recent MGS offering in February 2022, when the Treasury issued Malta Government Stocks once again at 4% but for 20-years as opposed to 10-years, demand from retail investors remained strong as well. In fact, a total of €91.3 million was applied for by retail investors. More surprising however was the fact that the 5-year bond at a yield of 3.24% was equally in strong demand by retail investors with applications amounting to €87.9 million.

It is evident from recent trends that there is a clear change in attitude by retail and corporate investors following the sharp upturn in yields. This change in investor behaviour is also instigating a number of banks to widely promote fixed deposits once again. Regular media promotions are taking place to encourage retail and corporate customers to subscribe for 2-year or 3-year deposits at 3% per annum.

However, investors need to compare the liquidity aspect of a fixed deposit when deliberating such an instrument as opposed to a T-Bill. Although Treasury Bills are normally held until their maturity date, holders of such securities have the facility of disposing of their holdings via the secondary market of the Malta Stock Exchange. The Central Bank of Malta (CBM), through the Government Securities Office, acts as ‘market-maker’ or ‘buyer of last resort’ for Malta Government Treasury bills in the secondary market with prices quoted on a daily basis for those investors requiring to liquidate before maturity. This is one key advantage of a Treasury bill as opposed to a fixed deposit at a bank.

The opportunity cost of holding excess liquidity lying idle without any return is now simply too large given the yield of 3% for money-market instruments which are easily accessible to the investing public.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.