Positive returns for MGS investors in 2023

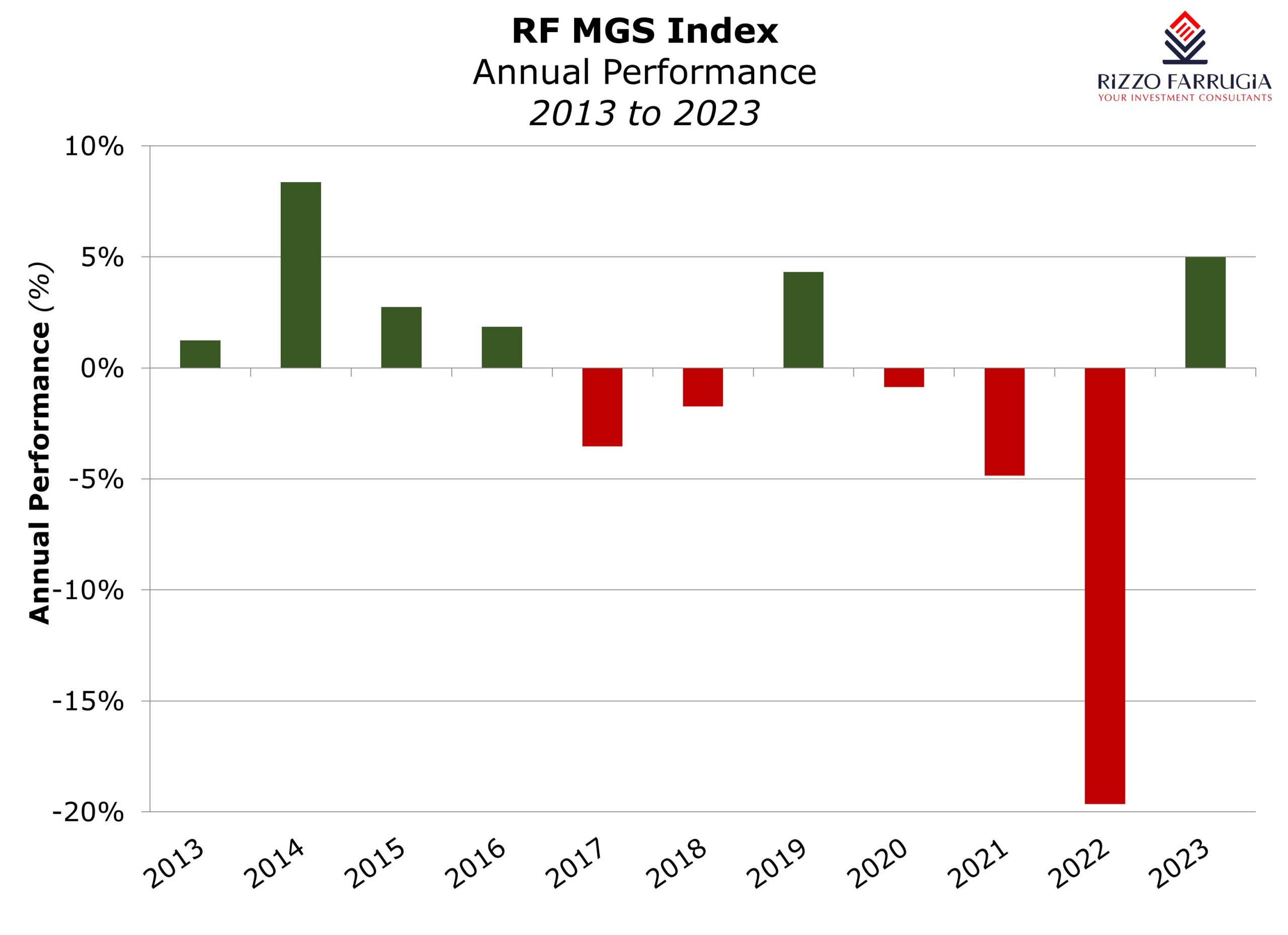

Malta’s sovereign bond market generated positive returns last year following three successive years of negative performances including the double-digit decline in 2022 which was brought about by the multiple interest rate hikes by the major central banks.

In 2023, the RF MGS Index, which is based on the Malta Government Stock bid prices published by the Central Bank of Malta on a daily basis, gained 4.99% – a welcome performance following the extraordinary 18.7% decline in 2022 which ranks as the worst annual performance on record for the MGS market as yields spiked.

Despite the overall positive performance for 2023, MGS prices experienced a high level of volatility throughout the year and the backdrop to the positive annual performance was the remarkable upward movement in the last few weeks of 2023. In fact, the RF MGS Index registered a fresh all-time low on 19 October 2023 as the major central banks were indicating that interest rates will remain ‘higher for longer’ in subsequent months. However, the RF MGS Index then rebounded strongly by more than 7.9% in the last 10 weeks of the year as investor sentiment across the international markets shifted abruptly on expectations of multiple rate cuts by the major central banks in 2024 following lower-than-expected inflation readings and weaker economic growth projections.

As I explained in some of my articles over recent years, in order to understand such important movements across the local and international bond markets, retail investors need to be aware of the differences between official interest rates set by the major central banks and secondary market bond yields which change on a daily basis. At times, these may be used interchangeably which could be rather confusing indeed.

Since financial markets are based on future expectations, as recent inflation readings in various parts of the world declined more-than-expected, sentiment shifted abruptly in November with investors focusing on the timing and overall size of interest rate cuts for 2024 and beyond. Although official interest rates by the Federal Reserve and the European Central Bank have not been changed bond yields dropped sharply in anticipation of future cuts in interest rates.

In fact, after reaching a multi-decade high of just over 3% in October, the German 10-year bond yield ended the year at the 2.03% level which was also reflected locally as the yield for the 10-year MGS ended the year at 3.13% compared to a multi-year high of 4.30% on 19 October. The sizeable drop in yields in such a short period of time is the reason for the rally in bond prices both internationally as well as across the MGS market.

The price movements in a number of individual MGS’s can help portray the rapid changes in a better manner. For example, the price of the 3% MGS 2040 which had dropped by just over 38 percentage points from 126.61% in December 2021 to 87.08% at the end of 2022 partly recovered to 93.84% at the end of 2023 after touching a level of 81.17% in October 2023. Likewise, the price of the 1.80% MGS 2051 (the 30-year bond launched in 2021) which sunk from 98.81% in December 2021 to 62.05% in December 2022 recovered to 66.70% at the end of 2023 after touching a level of 53.36% in October 2023.

During 2023, the Treasury tapped the market four times (February, July, September, and October) and issued a total of €1.39 billion (nominal) in new MGS’s. While retail investors were allowed to participate in the various securities issued in February, July and September, the last MGS issuance was restricted to institutional investors only via an auction. Retail investors had various options with some short-term offerings maturing in 3 years and 5 years as well as issuances of 10-year, 15-year and 20-year bonds.

Similar to the two examples above of MGS’s that had been issued several years ago, the prices of the new bonds issued throughout 2023 also fluctuated in line with movements across international bond markets. The longer-term MGS’s experienced wider fluctuations reflecting the effect of duration which implies that a drop in yields results in a higher price gain for longer dated securities. Moreover, the price volatility is also greater for bonds with lower coupons.

The 20-year MGS (the 4.00% MGS 2043) which was offered to investors at par (100%) in mid-February 2023 initially saw the indicative bid price rise to 104.89% in March 2023 before dropping to a low of 90.60% in October and ending the year at 105.58%. On the other hand, the 10-year MGS (the 4.00% MGS 2033) which was offered to investors at 100.75% in September 2023 dropped to a low of 97.56% in October before ending the year at 107.41%.

The 2024 Government Budget document had indicated that the MGS issuance for this year is expected to reach a record of €1.7 billion, which is intended to refinance existing debt of just under €500 million coupled with financing of €900 million for the deficit as well as €215 million as an equity investment earmarked for the new national airline. While the renewed upward movement in MGS prices is positive for investors who hold sizeable MGS’s in their portfolio, it may make it more challenging for the Treasury to issue such sizeable amounts at lower interest rates reflecting the current bond market yields with the 10-year MGS yield currently at 3.37%. Retail investor expectations may indeed take longer to adjust following such rapid movements in such a short period of time.

Movements across the bond markets are expected to remain volatile surrounding the publication of economic data and further statements by the major central banks ahead of any confirmation on timing and sizes of interest rate cuts. Following the sharp downward movements in bond yields in the last 10 weeks of the year, yields rose slightly since the start of the year on divergent views on the number of interest rate cuts projected by the ECB. Moreover, eurozone inflation data published late last week indicated that inflation rose from a two-year low of 2.4% in November to 2.9% last month while a measure of core inflation, which strips out volatile elements such as food and energy, still fell in December to 3.4% from 3.6% on an annual basis. Although there is widespread consensus that the major central banks will not need to hike rates any longer, the timing and sizes of interest rate cuts during the course of 2024 is still uncertain also due to ongoing geopolitical developments.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.