The Tick Size regime

In my article published two weeks ago, I gave an overview of some of the most important changes to procedures that investors need to be made aware of when dealing with investment services companies as a result of the introduction of MiFID II as from 3 January 2018.

The new legislation that was enacted across the EU last month also brought about some changes to the trading procedures for securities listed on the Malta Stock Exchange (MSE).

Prior to 3 January 2018, investors had the possibility of placing their orders in various methods on the system operated by the MSE. The most common alternative to the open order in the regular market was the hidden order which enabled investors to place bids or offers in all securities (whether equities, corporate bonds or Malta Government Stocks) which are not visible to other market players and investors, subject to a value of at least €50,000 or its equivalent amount (in a security which trades in a different currency). This enabled the larger investors to place sizeable bids or offers in an attempt to either purchase or dispose of large quantities without making the orders visible. In order to improve transparency, hidden orders as well as other less common types of orders (such as iceberg orders and midpoint orders) are no longer possible under MiFID II.

Meanwhile, the tick size regime, applicable for equities only, is another very important change under the new regulations which has wide-ranging implications for all investors dealing in equities on the MSE.

Article 49 of MiFID II requires trading venues (such as the Malta Stock Exchange) to adopt minimum tick sizes for equities. A tick size is the minimum price movement of a trading instrument. The minimum tick size regime depends on the liquidity and absolute price level of each of the equities.

Trading in equities on the MSE previously took place at any price subject to movements of €0.001. By way of example, an investor could either place a purchase or a sale order in Malta International Airport plc at say €4.899, €4.90, €4.901, €4.902, €4.903 etc. This €0.001 increment was possible in each of the equities on the MSE.

However, as from 3 January 2018, trading can only take place at specific tick sizes determined by reference to two criteria, namely the liquidity band and the market price band within which the equity is trading. This is governed by the Commission Delegated Regulation (EU) 2017/588 which establishes a harmonised tick size regime across the EU.

The new rule comprises six liquidity bands (depending on the average number of daily trades in a particular security) and 19 price ranges.

As a general rule, the tick size grows as liquidity declines and as a share price increases (in absolute terms). On the contrary, the tick size declines for lower share prices and improving liquidity. For example, assuming two equities within the same liquidity band with one priced at €8 and the other priced at €1.50, the tick size for the former is larger than that of the latter. Meanwhile, assuming two equities are both trading at €8 per share but one is more liquid than the other, the equity in which more trades are executed will have a smaller tick size.

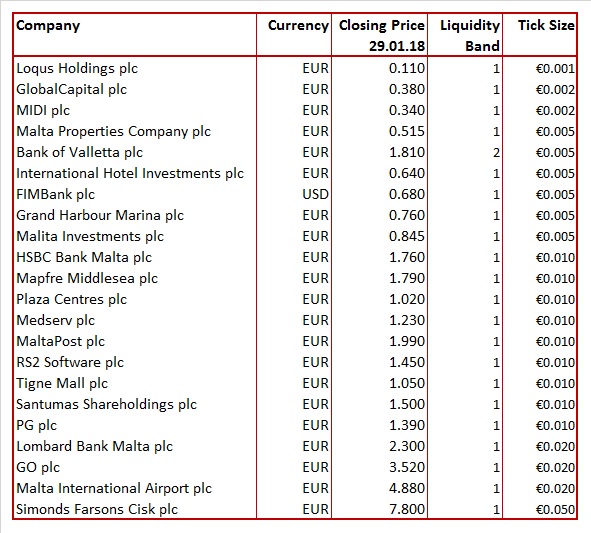

In Malta, all equities, with the exception of Bank of Valletta plc, fall within the lowest liquidity band since they did not register more than an average of 10 transactions per day. The MSE published a notice to all its members (stockbroking companies) on 28 December 2017 indicating the average daily number of trades in each security and the resultant tick size based on the liquidity band and the share price at the time. From the table presented by the MSE, it transpires that, no local equity (except BOV) registers more than an average of 5 trades per day.

Meanwhile, BOV falls within the second liquidity band (more than an average of 10 transactions per day but less than 80). The announcement by the MSE indicated that the equity of BOV registered an average of just over 13 trades per day.

In view of the fact that all equities except BOV are ranked in liquidity band 1, as indicated in the table, the minimum tick size varies depending on the absolute share price of each equity as opposed to previous tick size of €0.001 for any equity. The minimum tick sizes of GlobalCapital plc and MIDI plc are both €0.002 (since these shares are priced below €0.50), there are five other equities with a tick size of €0.005 (due to the absolute share prices being between €1.00 and €2.00), nine equities with a tick size of €0.01 (due to the absolute share prices being between €0.50 and €1.00), three equities with a tick size of €0.02 (namely Malta International Airport plc, GO plc and Lombard Bank Malta plc due to their absoliute share prices of between €2.00 and €5.00) and one equity (Simonds Farsons Cisk plc) with the largest tick size of €0.05 in view of its high absolute price of above €5.00 (currently at €7.80). As such, trades in the shares of Farsons can only take place in tick sizes of €0.05 such as €7.75, €7.80, €7.85, €7.90, etc.

The only equity that maintained the previous tick size is Loqus Holdings plc given its very low share price in absolute terms. However, this is hardly important for investors due to the very low level of trading in this equity which remains the only security listed on the Alternative Companies List and it never really generated a return to shareholders since its listing in the year 2000.

The minimum tick size of BOV is also €0.005 although the equity is priced between €1.00 and €2.00 since it is the only equity ranked in liquidity band 2.

The tick size automatically changes as a share price moves from one price band to another. This happened twice already during the first month of the year. Initally, when the share price of MIA hit a new record level of €5.00 on 17 January 2018, the next trade above this level could only take place in increments of €0.05 since the minimum tick size changed from €0.02 to €0.05. As such, for any trades above €5.00, only the following prices are possible €5.05, €5.10, €5.15, etc. Meanwhile, for any orders in the system below €5.00, the minimum tick size remained €0.02, thus trades can take place at €4.98, €4.96, etc.

Moreover, last Friday, the share price of Malta Properties Company plc surged by 15.5% to above the €0.50 level and the tick size also automatically changed from the previous level of €0.002 to €0.005.

Investors need to be aware of these tick sizes when submitting orders to their stockbrokers. Since the trading terminal will not accept incorrect tick sizes, the orders cannot be placed unless the client adjusts the limit price or the stockbroker amends it accordingly to the next available tick size.

Companies whose equities are listed on the MSE also need to be made aware of the tick size regime since a higher tick size is likely to reduce liquidity and potentially also increase the volatility of a particular equity. As such, some companies may wish to consider certain corporate actions, such as a share split, in order to reduce the absolute share price of their equity and hence the tick size with the aim of improving liquidity which is one of the primary reasons for gaining a stock exchange listing in the first place.

Assuming the level of trading activity in most equities remains within the first liquidity band (i.e less than an average of 10 trades per day), companies should aim to have their absolute share price at least below €2.00 (for a tick size of €0.01) or better still below €1.00 (to attain a tick size of €0.005). This should also be one of the considerations when new companies are contemplating an equity listing. Following the highly successful IPO of PG plc last year, other companies will hopefully also list their shares on the regulated main market of the MSE. Meanwhile, market players need to do their utmost to improve the liquidity across the equity market by attracting new investors for the benefit of all participants.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.