Tough year for Malta’s banks

As the 2020 annual reporting season comes to an end tomorrow, the banks whose shares or bonds are listed on the Malta Stock Exchange have all published their financial statements for last year.

A comparison of some key figures and financial indicators highlights some important findings which may be useful for the Maltese investing public. As expected, and in line with the circumstances also overseas, 2020 was indeed a tough year for the Maltese banking sector in general as all banks reported a significant reduction in profitability largely as a result of the spike in expected credit losses (“ECLs”) arising from the severe economic implications of COVID-19. The worst hit were MDB Group Ltd (which is the parent company of MeDirect Bank (Malta) plc and also one of the three local financial institutions which is directly supervised by the European Central Bank) and Bank of Valletta plc. Both MDB Group and Bank of Valletta recorded net impairment charges of just over €65 million. In the case of MDB Group, most of the bank’s charge emanated from its significant exposure to international lending as the Group only incurred an impairment charge of less than €0.4 million in relation to local lending and the Dutch mortgage business. On the other hand, a considerable part of BOV’s impairment charge amounting to almost €40 million was in relation to long outstanding non-performing loans (“NPLs”) as the bank explained that the current economic environment will continue to exacerbate the recovery process for the liquidation of assets (principally immovable property) held as collateral.

HSBC Bank Malta plc also recorded a marked increase in ECLs as these amounted to €25.6 million compared to just €0.39 million in 2019. In contrast, although all other local banks – namely Lombard Bank Malta plc, Izola Bank plc and APS Bank plc – took on additional impairment charges, these were more muted when compared to the multi-million losses suffered by the three largest financial institutions.

An important consideration which ought to be highlighted when analysing how local banks withstood the economic shock posed by COVID-19 is related to their level of capitalisation and liquidity which continued to strengthen even during such testing times. This development is also comforting for equity investors as the high level of capitalisation will help some of the banks return higher levels of capital to shareholders once the current restrictions by the European Central Bank are lifted. In fact, both HSBC Bank Malta and Lombard Bank Malta resumed dividend payments to shareholders albeit at levels far below those prior to the onset of the pandemic. On the other hand, the decision by Bank of Valletta not to declare a dividend for 2020 must also be seen in the context of the significant contingent liability amounting to €363 million in relation to the claim against it by the curators of the failed shipping line Deiulemar which is also a matter of interest for the overall stability of the entire Maltese financial system.

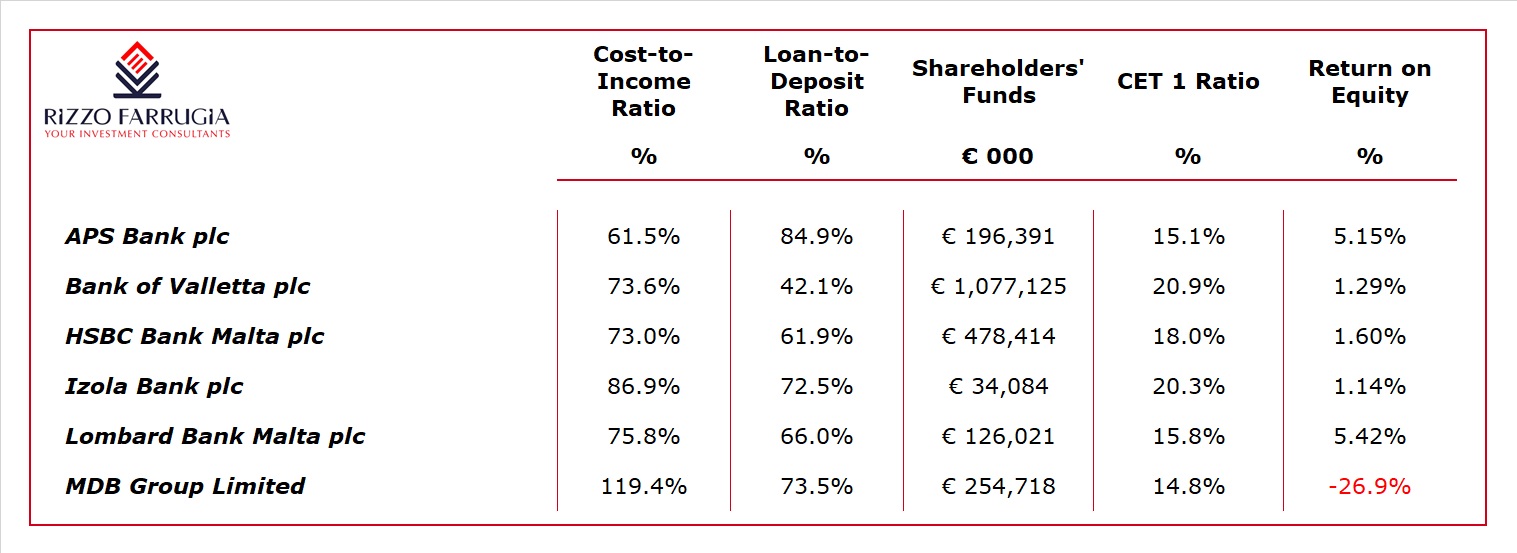

Indeed, Bank of Valletta remains by far Malta’s largest bank with total assets exceeding €12.9 billion which is almost twice as much as the amount held by Malta’s second largest bank – HSBC Bank Malta. However, just under 37% of the total assets of BOV are represented by customer loans amounting to €4.7 billion with the balance largely made up of financial assets and investments (€3.4 billion, or 26.7% of total assets) and short-term liquid funds (€4.3 billion, or 33.1% of total assets). In fact, an important metric when analysing banks is the level of loans compared to the deposit base which becomes even more critical in current circumstances due to the negative interest rate scenario which hugely dents the performance of those banks that have excess levels of liquidity. This is very much the case for BOV which has a particularly low loan-to-deposit ratio of 42.1%. In essence, this implies that less than half of the customer deposits are loaned out to personal or business customers through loans. On the other hand, the loan-to-deposit ratio of APS Bank is just under 85% which clearly shows the efficient management of the bank’s balance sheet with customer loans of €1.8 billion compared to customer deposits of €2.1 billion.

Another financial indicator that is regularly monitored among the banking sector is the cost-to-income ratio (or the ‘cost efficiency ratio’). The data for the 2020 financial year shows that this metric weakened across all banks as income was subdued as a result of the pandemic while costs continued to rise mainly reflecting increased regulatory costs and additional expenses related to digital transformation for some of the banks. The 2020 financial data indicate that APS Bank had the best cost-to-income ratio among the banks whose securities are listed on the MSE. The cost-to-income ratio of 61.5% was much stronger than that of the two largest banks, BOV and HSBC Malta, which almost had identical ratios of 73%. Meanwhile, MDB Group had a cost-to-income ratio in excess of 100% as total operating income contracted to €51.4 million in 2020 compared to the annualised figure of over €70 million in the previous nine-month period after the Group changed its accounting year-end from March to December in early 2019.

When analysing the cost-to-income ratio, it is worth highlighting that the consolidated financial statements of Lombard Bank Malta include the results of MaltaPost plc and therefore the comparison of certain line items with other banks may be somewhat misleading due to the inclusion of postal sales and revenue within the non-interest income of the Lombard Group, as well as the associated costs of the subsidiary. In fact, while the cost-to-income ratio at Group level is of 75.8%, the ratio at Bank level is much healthier at 52.4%. This would also rank Lombard Bank as the financial institution with the best cost-to-income ratio in Malta. When analysing the data over a number of years, it is evident that BOV’s cost-to-income ratio deteriorated the most as this increased from 45% in 2016 to 73.6% in 2020.

As a result of the extremely challenging conditions which resulted in a sharp rise in ECLs, the overall profitability levels of each of the banks declined markedly in 2020. The most profitable bank in absolute terms remained BOV with a profit after tax of €13.8 million (2019: €63.5 million) followed by APS Bank with a profit after tax of €9.9 million (2019: €19.1 million) and HSBC Malta (€7.6 million). However, the most important profitability ratio is the return on equity comparing the profit after tax with the average shareholders’ funds. Due to the large amount of shareholders’ funds within BOV’s balance sheet at over €1 billion, the return on equity was a paltry 1.29% in 2020. Although one should not expect BOV’s return on equity to return to double-digit figures in the years ahead as many investors were accustomed to before the start of the global financial crisis in 2008 when the regulatory environment and the interest rate scenario were totally different than today’s situation, it would be reasonable to expect more adequate returns on equity from the banks in future years. The highest returns on equity in 2020 were registered by Lombard Bank at 5.4% closely followed by APS Bank at 5.2%. While it is worth pointing out that the return on equity for APS was 11.7% in 2019, it was below the 10% level in earlier years as the bank’s performance in 2019 was boosted by the realised and unrealised gains made on financial instruments as well as the record income generated from fees and commissions and the associate company operating in the fund business. Likewise, Lombard’s return on equity has been below the 10% level since 2010 as operating expenses almost doubled during this period whilst Lombard’s equity base grew markedly to €126 million compared to €71.7 million as at the end of 2010.

As highlighted earlier on, the capitalisation levels of all banks remained robust despite the challenging circumstances and the high amount of ECLs that were incurred in 2020. The Common Equity Tier 1 ratio and the Total Capital ratio are very closely watched indicators by professional investors, regulators and credit rating agencies. It is therefore very comforting to note that BOV’s CET 1 ratio exceeded the 20% level in 2020. This must however also be seen in the context of the very large pending litigation case being faced by the bank and, as such, it should be expected that such high levels of capital would need to be maintained until this litigation case is resolved. It is also noteworthy to highlight that HSBC Malta had a CET 1 ratio of 18% as at December 2020 which is the highest level ever and is also indicative of the probability of more attractive dividends that may flow to shareholders once regulator restrictions are lifted. Meanwhile, in its 2020 Annual Report, APS Bank once again made reference to its Capital Development Plan whereby the bank explained that in 2022, it will “campaign to raise what would be the largest-ever round of capital for APS Bank.” Following the successful issuance of €55 million in new subordinated bonds in late 2020, a new capital raising exercise by APS Bank promises to be another defining moment for the bank as it seeks to expand its business and outreach in line with its growth objectives.

Following the recent acceleration of the vaccine rollout in Malta and the re-opening of the tourism sector as from 1 June 2021, it would be interesting to gauge the extent of the economic recovery during the summer months and how this may impact the non-interest income and the ECLs at the various banks. This could be one of the determining factors for the banks to report more meaningful profitability levels and hopefully higher dividends to shareholders.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.