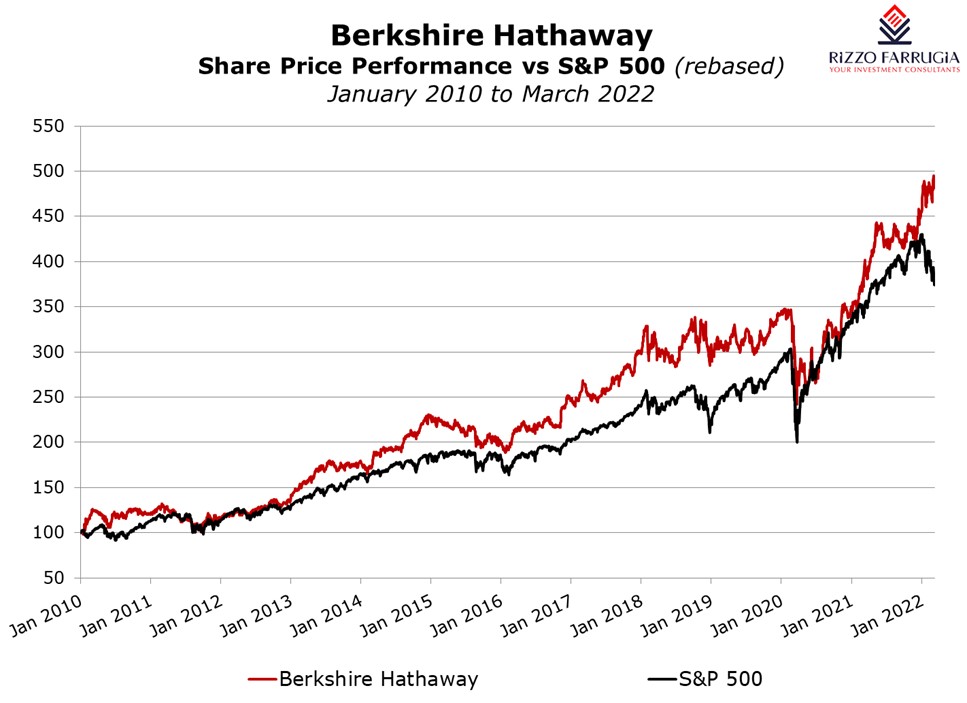

Warren Buffett & the benefit of share buybacks

On Saturday 26 February, Berkshire Hathaway Inc – the investment conglomerate run by legendary investor Warren Buffett – published its annual letter to shareholders in conjunction with the publication of its 2021 financial statements.

Warren Buffett’s annual letter is a widely-anticipated publication by the international financial media since it always has some key messages to the investment community around the world.

In the most recent letter, Warren Buffett gives an overview of the current structure of the investment conglomerate and also highlights the availability of USD144 billion in cash. While he reiterates his pledge that Berkshire will always maintain a healthy cash balance to enable the company to be “financially impregnable”, the Chairman acknowledged that the overweight cash holding is “as a consequence of my failure to find entire companies or small positions thereof which meet our criteria for long-term holding”.

In the introduction to the letter, Warren Buffett explains that Berkshire owns a variety of businesses, either in their entirety or by acquiring minority stakes in publicly traded companies with the largest positions of the latter group being Apple Inc (December 2021 market value of USD161.2 billion), Bank of America (USD45.6 billion), American Express Company (USD24.8 billion) and The Coca Cola Company (USD23.7 billion) among numerous other.

The Chairman of Berkshire highlights the investment philosophy as follows: “we own stocks based upon our expectations about their long-term business performance and not because we view them as vehicles for timely market moves”. In fact, he claimed that they are not stock-pickers but they are “business-pickers”. In fact, Warren Buffett also states that irrespective of whether they own a business as a whole or participate as a minority shareholder “our goal is to have meaningful investments in businesses with both durable economic advantages and a first-class CEO”.

Despite the inability for Berkshire to deploy a large part of its cash balance over recent years, Warren Buffett still claims that they found a “a mildly attractive alternative during 2020 and 2021 for deploying capital” apart from the primary objective of increasing the “long-term earning power” of those business fully-controlled by Berkshire Hathaway.

Warren Buffet is referring to the share buyback programme conducted by Berkshire Hathaway. During 2020 and 2021, the company repurchased 9% of its own shares that were outstanding at the end of 2019 for a total cost of USD51.7 billion. Moreover, during the first two months of 2022, additional shares were repurchased for a total of USD1.2 billion.

The Chairman explains that through this share buyback programme, the effective ownership of the underlying investments held by the company increases for the remaining shareholders. Warren Buffett adopts a diligent approach on the timing of share buybacks and he states that “for Berkshire repurchases to make sense, our shares must offer appropriate value”. He argues that as Berkshire seeks to avoid overpaying when conducting acquisitions of other companies, “it would be value-destroying if we were to overpay when we are buying Berkshire”.

Warren Buffett also claims that “when the price/value equation is right, this path is the easiest and most certain way for us to increase your wealth”.

Many of the large multinationals in the US and Europe conduct such share buybacks along customary cash dividends. In fact, in the recent letter Warren Buffett also praised Apple’s CEO Tim Cook for utilising part of Apple’s large cash pile to also repurchase outstanding shares. This enabled Berkshire to increase its equity stake in Apple to 5.55% from 5.39% a year earlier without conducting any additional purchases. While he highlighted that the change in the minority stake may seem to be small, Warren Buffett argued that “each 0.1% of Apple’s 2021 earnings amounted to USD100 million”.

Share buybacks are an effective way of distributing excess cash to shareholders. In Malta, only one company has so far conducted a share buyback. This was Plaza Centres plc when during the third quarter of 2020, it declared its intention to repurchase up to 10% of its issued share capital following the sale of one of its properties.

Although few Maltese companies may have sufficient financial resources to conduct such share buybacks, another issue that might prohibit companies from carrying out such a corporate action would be the free float restriction imposed by the Listing Authority. This ought to be another reason for decisive action to be taken on the minimum 25% free float threshold.

In view of the very illiquid nature of the Maltese capital market which essentially makes it very difficult for large shareholders to liquidate part of their position or crystallise capital gains accumulated across the years in a short period of time, a share buyback could prove to be a good strategy to inject liquidity into the market.

Print This Page DisclaimerThe article contains public information only and is published solely for informational purposes. It should not be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in this article. Rizzo, Farrugia & Co. (Stockbrokers) Ltd (“Rizzo Farrugia”) is under no obligation to update or keep current the information contained herein. Since the buying and selling of securities by any person is dependent on that person’s financial situation and an assessment of the suitability and appropriateness of the proposed transaction, no person should act upon any recommendation in this article without first obtaining investment advice. Rizzo Farrugia, its directors, the author of this article, other employees or clients may have or have had interests in the securities referred to herein and may at any time make purchases and/or sales in them as principal or agent. Furthermore, Rizzo Farrugia may have or have had a relationship with or may provide or has provided other services of a corporate nature to companies herein mentioned. Stock markets are volatile and subject to fluctuations which cannot be reasonably foreseen. Past performance is not necessarily indicative of future results. Foreign currency rates of exchange may adversely affect the value, price or income of any security mentioned in this article. Neither Rizzo Farrugia, nor any of its directors or employees accepts any liability for any loss or damage arising out of the use of all or any part of this article. Additional information can be made available upon request from Rizzo, Farrugia & Co. (Stockbrokers) Ltd., Airways House, Fourth Floor, High Street, Sliema SLM 1551. Telephone: +356 2258 3000; Email: info@rizzofarrugia.com; Website: www.rizzofarrugia.com © 2021 Rizzo, Farrugia & Co. (Stockbrokers) Ltd. All rights reserved. This article may not be reproduced or redistributed, in whole or in part, without the written permission of Rizzo Farrugia. Moreover, Rizzo Farrugia accepts no liability whatsoever for the actions of third parties in this respect.

This article was produced by Edward Rizzo, Director at Rizzo Farrugia, which is a company licensed to undertake investment services in Malta by the MFSA under the Investment Services Act, Cap. 370 of the Laws of Malta and a member of the Malta Stock Exchange. The company’s registered address is at Airways House, Fourth Floor, High Street, Sliema SLM 1551, Malta.